If you’re turning 65 soon and have been studying your Medicare options, one plan you’ve probably heard about is Medicare Supplement Plan G (Medigap G).

Medigap Plan G is one of the most popular Medicare Supplement Plans today. On social media, you’ll often find it endorsed as one of the “best” Medicare plans.

However, Medigap Plan G also comes with a pretty hefty price tag and doesn’t cover a few key healthcare expenses, which causes many people to hesitate.

If you compare Medicare Supplement Plan G with your other options on Medicare’s website, you might feel that the information is lacking.

It doesn’t provide you with a clear picture of how much you’ll actually spend with a Medigap G, and all the caveats that you need to be aware of with this plan.

But don’t stress, we’re here to help.

In this article, we’ll go over what exactly Medicare Supplement Plan G is, what it covers and what it doesn’t cover, how much it costs, and give you a pros and cons list for this plan.

| Medicare Supplement Plan G Through the Eyes of “Jack” To help you better understand whether Medicare Supplement Plan G is the right plan fit for you, we’re going to take a look at how someone might approach enrolling in this plan and the key things to consider. Our “hero” for today is Jack, a 64-year-old man who is about to turn 65 in six months. Jack was also recently diagnosed with cancer, so he is anticipating costly medical bills in the following years. Jack has been recently studying anything he could find about Medicare. But even after hours of reading, he finds himself still confused about which plan to sign up for. One thing he did notice, however, is that many people online suggest enrolling in a Medicare Supplement Plan G. Curious about this, he decides to take a closer look… |

What is Medicare Supplement Plan G?

Plan G is one of ten Medicare Supplement Plans that Medicare beneficiaries can enroll in for lower out-of-pocket expenses. It is one of the most popular Medicare Supplement Plans (Medigap plans) today and is considered by some as the most simple and easy-to-understand plan.

When you enroll in Original Medicare (Medicare Parts A and B), Medicare will cover roughly 80% of your healthcare costs, while you’re typically responsible for paying the remaining 20% out-of-pocket.

Because there’s no limit to the 20% that you’re responsible for paying, your out-of-pocket expenses can potentially get very high without additional coverage. That’s why many people also choose to enroll in either a Medicare Supplement Plan or a Medicare Advantage Plan.

What are Medicare Supplement Plans?

Medicare Supplement Plans are secondary insurance to Original Medicare. They are provided by private insurance companies, and they are designed to pay for some of the out-of-pocket of Original Medicare.

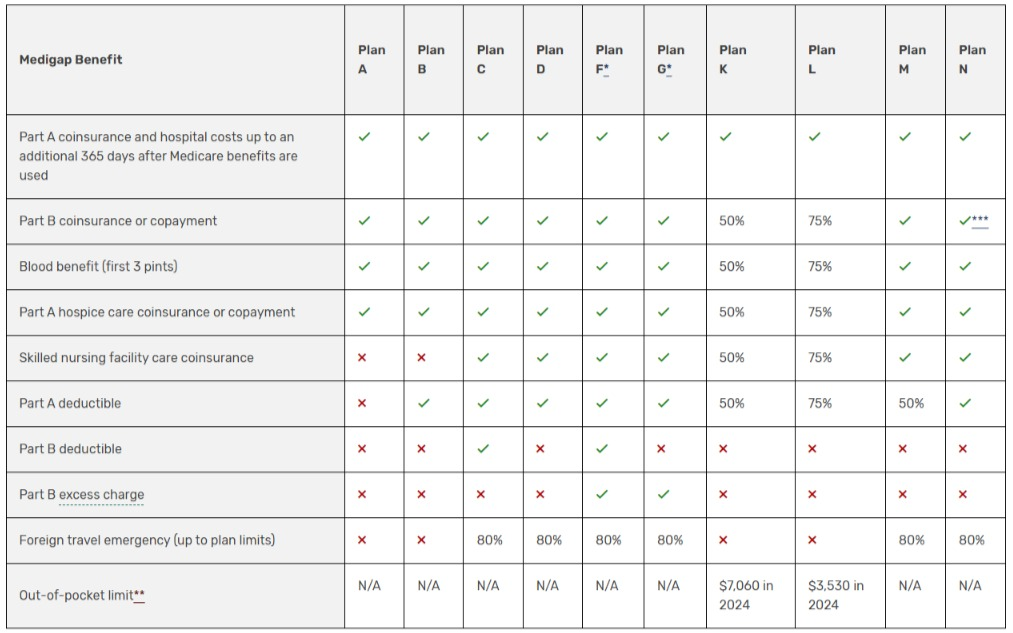

There are ten Medicare Supplement Plans today (namely Plan A, B, C, D, F, G, J, K, L, M, and N). These plans are standardized, meaning that you’ll get the same coverage for a Medicare Supplement Plan G (or Plan N or any other of the ten plans) regardless of which insurance company you get it from.

| Learning About Medicare Supplement Plans To understand what Medicare Supplement Plan G is, Jack first got a firm grasp of how Original Medicare works, and why most people get additional coverage. Once he fully understood that, he began studying what exactly Medicare Supplement Plans are. While doing this he noticed that the two most popular Medicare Supplement Plans today are Medigap Plan G and Plan N. Eager to learn more, he started comparing the two plans… |

What Does Medicare Supplement Plan G Cover?

Medicare Supplement Plan G covers most of the gaps in Original Medicare. This includes the following:

- Medicare Part A Deductible – The amount you have to spend out-of-pocket first before Medicare Part A starts covering you. In 2025, the Medicare Part A deductible is set to $1,676 per benefit period.

- Medicare Part A Hospital Copays – The daily copays you have to pay if you’re admitted to a hospital for more than 60 days. In 2025, this is $419/day for days 61 – 90, $838/day for days 91 – 150 (using lifetime reserve days), and 100% of the bill if you stay longer than 150 days.

- Skilled Nursing Facility Copays – The daily copays you pay if you’re admitted to a skilled nursing facility for more than 20 days. In 2025, you pay $209.5/day for days 21 – 100 in an SNF, and 100% of the bill if you stay longer than 100 days.

- Medicare Part B Coinsurance – The 20% you’re generally responsible for paying for most items and services covered by Medicare Part B.

- Medicare Part B Excess Charges – If a healthcare provider takes Medicare, but doesn’t accept the Medicare-approved amount, they may charge up to 15% more than the Medicare-approved amount. Without additional coverage, you’re responsible for paying this excess charge out-of-pocket.

- First Three Pints of Blood – If you have to purchase blood, Original Medicare generally won’t cover the first three pints. However, Medicare Supplement Plan G will cover this for you.

- Foreign Travel Emergencies – If you’re traveling outside the United States and have a medical emergency, Medicare Supplement Plan G will cover 80% of your costs up to a lifetime maximum of $50,000.

What Does Medicare Supplement Plan G Not Cover?

Medicare Supplement Plan G does not cover the Medicare Part B deductible or most items or services that Original Medicare doesn’t cover.

- Medicare Part B Deductible – The amount you have to spend out-of-pocket first before Medicare Part B starts covering you. In 2025, the Medicare Part B deductible is set to $257.

- Items and services not covered by Original Medicare – Most items and services that Original Medicare doesn’t cover, Medicare Supplement Plan G also won’t cover. This includes most prescription drugs, long-term care, and routine dental, vision, and hearing care.

| Learning What Medicare Supplement Plan G Covers When Jack started looking at what Medicare Supplement Plan G covers, he was excited! He realized that if he enrolled in Medicare Supplement Plan G, most of his cancer treatment expenses would be covered. The only out-of-pocket expense he would have to pay is the Medicare Part B deductible, which is set to $257 in 2025. While looking at this, he also realized that this is why Medicare Supplement Plan G is so popular—many people prefer not having to worry about high out-of-pocket risk. |

How Much Does Medicare Supplement Plan G Cost?

The cost of Medicare Supplement Plan G depends on several factors, including your age, gender, location, the insurance company selling the plan, whether you use tobacco or qualify for a household discount, and several other factors.

Generally speaking, Medicare Supplement Plan G often has higher premiums than most other Medicare Supplement Plans (including Plan N, which is another popular Medicare Supplement Plan).

Medicare Supplement Plan G is also often more expensive than Medicare Advantage Plans, which can sometimes have $0 premiums.

To help you have a better idea of how much the monthly premiums for Medicare Supplement Plan G are, here are some price range estimates taken from different cities around the United States:

| Medicare Supplement Plan G | Medicare Supplement Plan N | |

| New York City, New York | $302 – $776 | $220 – $483 |

| Indianapolis, Indiana | $114 – $493 | $86 – $496 |

| Los Angeles, California | $148 – $278 | $114 – $213 |

*Price estimates above are taken from Medicare.gov for a 65-year-old male who doesn’t use tobacco and doesn’t qualify for household discounts. To get accurate quotes in your area, call or text us at +1 877-360-6565 (TTY: 711)

| Cost of Medicare Supplement Plan G Jack’s excitement with Medicare Supplement Plan G took a hit when he saw how much it cost. Jack lives in a zip code where the average price of Plan G is $150/month. Jack decided to do some calculations and realized that if he enrolled in an average Medicare Supplement Plan G in his area, he would end up spending $4,020/year on Medicare for his Medicare Part B premium ($185 in 2025) and Medicare Supplement Plan G premium only. That’s even without getting any healthcare services! Jack realizes that this is one of the main reasons why not everyone goes for Medicare Supplement Plan G. The coverage seems great, but the price can be heavy for many people. |

Pros and Cons of Medicare Supplement Plan G

| Pros | Cons |

| Covers most of the gaps in Original Medicare Easy-to-understand and predictable costs Covers you for any doctor or healthcare provider that accepts Medicare | More expensive than other plan options Doesn’t include prescription drug coverage or other benefits not included in Original Medicare |

A recent report by the AHIP shows that 36% of people who choose to enroll in a Medicare Supplement Plan enroll in a Plan G. This makes it the second most popular Medicare Supplement Plan just behind Plan F (which the same AHIP report shows is becoming less popular every year).

Here are some reasons we see people choosing to enroll in a Medicare Supplement Plan G, and some reasons we see people avoid this plan.

Pro: Covers Most of the Gaps in Original Medicare

Medicare Supplement Plan G covers the Medicare Part A deductible and copays, the Medicare Part B coinsurance and excess charges, and it also covers the first three pints of blood if you need to purchase it, and foreign travel emergencies.

Compared to other plans, only Medicare Supplement Plan F covers more gaps in Original Medicare than Plan G (and Plan F isn’t available anymore for people who turn 65 on or after January 1, 2020).

This is why people who prefer to have low out-of-pocket expenses with Medicare are often drawn to Medicare Supplement Plan G. If ever these people have a year with plenty of health issues, their Medicare Supplement Plan G should take the brunt of the medical bills!

Con: More Expensive Than Other Plan Options

Some people might want to get a Medicare Supplement Plan G, but its hefty price tag is simply too much for their budget and lifestyle. The exact price of Medicare Supplement Plan G varies by location and on several factors, but it’s generally one of the more expensive Medicare plans.

Note: To find out how much Medicare Supplement Plan G costs in your area, call or text our team of licensed insurance agents at +1 877-360-6565 (TTY: 711), and we’d be glad to assist you at no cost to you!

Pro: Easy-to-understand and Predictable Costs

Another reason we see people choosing Medicare Supplement Plan G is because it’s easier to understand and budget compared to other plans.

Yes, the premiums are often higher than other plan types, but since there are relatively fewer out-of-pocket expenses (only the Medicare Part B deductible), you should be able to budget how much you’re going to spend for your healthcare in a year relatively easily—regardless if it’s a year with few health issues, or a year with plenty of health issues.

If you take a look at other plans like Medicare Supplement Plan N or a Medicare Advantage Plan, you’ll find that there are generally more cost variables. Medicare Supplement Plan N has copays for when you visit a doctor or ER, while Medicare Advantage Plans usually set different copays for different items and services.

Con: Doesn’t Include Prescription Drug Coverage and Others

Because Medicare Supplement Plans are secondary insurance to Original Medicare, they generally don’t cover items and services not covered by Original Medicare.

That’s why Medicare Supplement Plan G doesn’t cover prescription drugs, long-term care, and routine dental, vision, and hearing care.

People who enroll in a Medigap Plan G often also enroll in a standalone Medicare Part D plan to cover their prescription drug costs. Medicare Part D prescription drug plans have their own premiums, deductibles, and copays—which adds more costs and is another reason some people can’t afford to go for a Medicare Supplement Plan G.

Pro: Covers You For Any Doctor That Takes Medicare

Another reason some people choose a Medicare Supplement Plan G despite its higher costs is because they can go to any doctor or healthcare provider that takes Medicare, and their Plan G should cover them.

This is unlike Medicare Advantage Plans, which often have networks of doctors and hospitals where beneficiaries can get low-cost healthcare. However, if beneficiaries get services outside their Medicare Advantage Plan’s network, they may not be covered (most HMO plans), or may have to pay higher copays (most PPO plans).

With a Medicare Supplement Plan G, you typically won’t need referrals to see a specialist or prior authorizations for special treatment. Most of the time, if your doctor deems a procedure medically necessary, your Medicare Supplement Plan G should cover it.

| Weighing the Pros and Cons When Jack first saw the price of Medicare Supplement Plan G, he felt a bit discouraged. He felt even more discouraged when he realized that he’d have to enroll in a standalone Medicare Part D prescription drug plan as well since Medicare Supplement Plans don’t cover prescription drugs. However, he decided to do a double-take. He took a close look at Medicare Supplement Plan G again, and compared it to his other options—and he realized that there are indeed plenty of pros to enrolling in Plan G. Jack especially likes that he can see any doctor that accepts Medicare. Jack lives in a rural area, so his options are pretty limited already. With a Medicare Supplement Plan G, he can go to any healthcare facility that takes Medicare. |

Who is Medicare Supplement Plan G Popular With?

Medicare Supplement Plan G is generally popular with people who want predictable healthcare costs and don’t mind the higher premiums.

People who have plenty of health issues also tend to lean towards plans that have low out-of-pocket expenses such as Medicare Supplement Plan G. Even with higher premiums, Medicare Supplement Plan G can potentially save some people money because of its low out-of-pocket risk.

Other people prefer Medicare Supplement Plan G because of its predictable costs. Medicare Supplement Plan G is one of the easier plans to understand. That’s why some people with few health issues still choose to pay more for a Medicare Supplement Plan G than other plan types because they prefer the peace of mind that Plan G gives them.

| Jack’s Decision After carefully considering all the options, Jack decides he is going to enroll in a Medicare Supplement Plan G. He isn’t the wealthiest person, so the $150/month he has to pay for Medicare Supplement Plan G in his area does affect his wallet. However, he realizes that he’s probably going to need the coverage that it provides for his upcoming cancer treatment. Also, the Medicare Supplement Plan G allows him to get cancer treatment anywhere that accepts Medicare. If ever he needs to see a specialist in a different state, his Plan G should still cover him. |

Frequently Asked Questions About Medicare Supplement Plan G

How Do You Enroll in Medicare Supplement Plan G?

To enroll in a Medicare Supplement Plan G, you must be enrolled in both Medicare Parts A and B. Once you’re enrolled in Original Medicare, there are generally two ways you can enroll in a Medicare Supplement Plan G:

- Research and compare plans in your area on your own, then contact the insurance company you want to sign up with once you’re ready to enroll, or

- Contact a licensed insurance agent for help comparing your options, and getting assistance from them to enroll at no cost to you.

Licensed insurance agents contract with several different insurance companies, so they can be unbiased when helping you choose a plan. Licensed insurance agents are also paid by commission, so you can get their services without paying anything!

Note: need help finding the right Medicare Supplement Plan G for you in your area? Call or text our team at +1 877-360-6565 (TTY: 711).

Can You Enroll in Medicare Supplement Plan G At Any Time?

It depends on your health condition.

Everyone gets one period where insurance companies selling Medicare Supplement Plans must take you in regardless of your health condition (they also cannot charge you more than the preferred rate). This is known as the Medigap Open Enrollment Period, and it runs for six months starting when your Medicare Part B coverage takes effect. If you enroll in a Medicare Supplement Plan G during your Medigap Open Enrollment Period, you are guaranteed to get the plan.

However, if you enroll in a Medicare Supplement Plan G outside the Medigap Open Enrollment Period, you may be subject to medical underwriting. The insurance company will usually ask you several health-related questions, and they can deny your application if you don’t pass their criteria.

That’s why it’s generally a good idea to study your options before you enroll in Medicare. This way, if you find that Medicare Supplement Plan G is the right fit for you, you can enroll during your Medigap Open Enrollment Period, and won’t have to worry about passing medical underwriting.

Can You Switch From a Medicare Advantage Plan to Medicare Supplement Plan G (and vice versa)?

Yes, you may switch from a Medicare Advantage Plan to a Medicare Supplement Plan G, but you may need to pass medical underwriting if you switch outside your Medigap Open Enrollment Period.

There are a few special cases where you can switch from a Medicare Advantage Plan to a Medicare Supplement Plan outside the Medigap Open Enrollment Period without undergoing medical underwriting. These are known as Guaranteed Issue Rights situations.

One example of a Guaranteed Issue Right situation is if you enroll in a Medicare Advantage Plan when you’re first eligible for Medicare, you have one year to switch to a Medicare Supplement Plan without medical underwriting. Another Guaranteed Issue Right situation is if your Medicare Advantage Plan leaves Medicare.

You may visit Medicare’s website to learn more about other Guaranteed Issue Rights situations.

If you don’t qualify for Guaranteed Issue Rights, you can generally drop your Medicare Advantage Plan and apply for a Medicare Supplement Plan G (with medical underwriting) during the Annual Enrollment Period (October 15 – December 7) or the Medicare Advantage Open Enrollment Period (January 1 – March 31) every year.

Can You Switch Between Medicare Supplement Plans?

Yes, you can generally switch between Medicare Supplement Plans if you pass medical underwriting or qualify for guaranteed issue rights.

What Are Popular Alternatives to Medicare Supplement Plan G?

Two popular alternatives to Medicare Supplement Plan G are Medicare Supplement Plan N and Medicare Advantage Plans.

According to the AHIP’s report on Medicare Supplement Plans, Plan N is the third most popular Medicare Supplement Plan.

Medicare Supplement Plan N generally has lower premiums than Plan G. However, it has copays for doctor and ER visits, and it doesn’t cover Medicare Part B excess charges. People who enroll in Medicare Supplement Plan N have slightly more out-of-pocket risk than those who enroll in Plan G.

Medicare Advantage Plans are another option that many people go for. We found that many people who find Medicare Supplement Plan G to be too expensive often choose a Medicare Advantage Plan instead. This is because many Medicare Advantage Plans have low to $0 premiums.

Medicare Advantage Plans are not standardized, so each plan is free to set its own premium, deductible, and copays. Generally speaking, Medicare Advantage Plans have lower premiums than Medicare Supplement Plan G but may have higher out-of-pocket risk.

Conclusion – Should You Enroll in Medicare Supplement Plan G?

| Jack Enrolls in Medicare Supplement Plan G! After doing lots of research and weighing the pros and cons, Jack finally decides to enroll in Medicare Supplement Plan G. After enrolling in Medicare Parts A and B three months before turning 65, he then contacts PlanFit for help finding the right Medicare Supplement Plan G for himself. With the PlanFit agents’ help, Jack is able to find a plan that he’s happy with. Jack also decides to enroll in a Medicare Part D prescription drug plan, so the PlanFit agent also helps find a plan that covers his prescription drugs at the lowest price! |

Medicare Supplement Plan G is one of the most popular plans today. However, in Medicare, there’s no such thing as the “best” plan, there’s only the best plan for you.

By reading this article, we hope that you have a much better idea of how Medicare Supplement Plan G works, what it covers, how much it costs, and whether or not it suits your specific lifestyle.

Now, that you know the basics of Medicare Supplement Plan G, the next step is to go and take a closer look at the Plan Gs available in your area. If you need help with this, don’t hesitate to call or text us at +1 877-360-6565 (TTY: 711)!

Calvin Bagley is the founder of PlanFit, The Medicare Store, and Nuvo Health. He and his team have helped over 60,000 people navigate Medicare options, and he’s a nationally recognized speaker in the Medicare industry. Most importantly, he’s someone who believes every American deserves clear, honest information without pressure.