- Medicare Part D is the branch of Medicare that covers your prescription drug costs. It’s provided by private insurance companies that are approved by Medicare.

- Medicare Part D is NOT included in Original Medicare (Part A and B). You must enroll in Part D separately as a standalone plan or as part of a Medicare Advantage Plan

- You may have to pay premiums, deductibles, copays, and coinsurances out-of-pocket.

- Generally speaking the maximum out-of-pocket amount for 2026 is $2,100.

- You can enroll in a Part D plan when you first become eligible for Medicare. If you miss your Initial Enrollment Period, you may incur permanent penalties on your premiums.

Medicare Part D is easily one of the most confusing parts of Medicare.

There are so many regulations and variables surrounding it that it can be quite overwhelming.

And if you don’t get it right, you can even get permanent penalties that you have to pay for the rest of your life.

But don’t worry!

Today, I’m going to simplify Medicare Part D for you.

As the former CEO of Nuvo Health and The Medicare Store, I’ve helped thousands of seniors get the best drug coverage for themselves.

Let’s start with definitions.

What Are Medicare Part D Plans?

Medicare Part D is the branch of Medicare that covers prescription drugs. These plans are provided by private insurance companies, and you enroll in one separately from Medicare Part A and B.

Original Medicare (Part A and B) doesn’t cover most prescription drugs. That’s why Part D was created – so you can get coverage for one of the most expensive sides of healthcare.

You are not required to enroll in Medicare Part D. But if you’re aged 65 or over, and you go without creditable drug coverage, you may incur penalties when you do decide to enroll in Part D (more on this later).

You can enroll in a standalone Part D Plan, or you can get a Medicare Advantage Plan that has Part D built into it.

What Does Medicare Part D Cover?

Medicare Part D plans typically cover both generic and brand-name drugs. Providers must adhere to some regulations, but they can largely create their own formularies and decide which drugs to include.

One regulation all plans must stick to is to include at least two drugs for each drug category.

By drug category, I mean drugs that treat the same symptoms or have the same effects. Providers can choose the exact drugs they cover, but they need to include at least two per category.

Another regulation is that all plans must include all drugs in the following protected categories:

- Anticancer drugs

- Anticonvulsive treatments

- Antidepressants

- Antipsychotic medications

- HIV/AIDS treatments

- Immunosuppressant drugs

So, if you’re taking medication that falls under one of those protected categories, finding a plan that covers your prescription meds shouldn’t be difficult.

Finally, Part D drug plans are also required to cover most vaccines.

Are There Prior Authorizations For Medicare Part D?

Often, yes. For some tiers of drugs, your plan provider may impose prior authorizations and/or other coverage rules like step therapy or quantity limits.

They do this to ensure that you don’t just use your plan to get a bunch of drugs that you don’t really need.

For most generic drugs, these won’t be necessary. But when it comes to the more expensive drugs, there are usually some of these coverage rules in place.

- Prior Authorizations: Sometimes, your doctor or prescriber needs to prove to your plan provider that the drug is medically necessary. If the plan provider accepts, you can use your plan to cover the costs of your prescribed medications. If they reject, you’ll typically pay for the drugs out-of-pocket or switch to another drug that your provider accepts.

- Step Therapy: Sometimes, your plan provider will ask you to try taking a generic drug first before they cover a more expensive brand-name drug. If your doctor or prescriber believes this is unnecessary or dangerous, you may request an exemption from step therapy.

- Quantity Limits: Some drug plans put quantity limits on certain drugs. This means they’ll only cover a certain amount. If you purchase more than the limit, then they’ll no longer cover the costs. However, if your doctor or prescriber deems the limit too low, you can request an exemption from the quantity limit. Additionally, the max out-of-pocket for a given year is $2,100 in 2026.

The coverage rules vary from provider to provider.

But generally speaking, if your doctor sees that it’s medically necessary for you to go against your plan’s coverage rules, you can request an exemption from your plan provider. Whether they honor the exemption or not is up to your plan provider.

How Much Does Medicare Part D Cost?

The average cost for a Part D drug plan is $34.50/month in 2026. However, there are also deductibles, copays, and coinsurances. Each provider sets their own cost-sharing terms.

- Premiums are the monthly payments you make to your plan provider to keep the plan. These range from $0 – $200/month depending on coverage and location.

- Deductibles are the amount you spend for drugs out-of-pocket before your coverage begins. Your provider is free to choose the deductibles for their plans, with some having $0 deductibles. However, the limit for deductibles in 2026 is $615/year.

- Copays are a cost-sharing method. You pay a set amount for each drug, while your insurance provider covers the remaining cost. Ex: if you have a $20 copay for a $100 drug, you pay the $20, while your provider covers the remaining $80. Plan providers are free to set their own copay amounts. Most do this in tiers (more on this below).

- Coinsurance is another cost-sharing method. Instead of giving you a fixed amount to pay, you pay a percentage of the cost. Ex: if you have a 25% coinsurance for a $100 drug, you pay $25, while your provider covers the remaining $75. Plans can set their own coinsurance amounts, and most do this in tiers.

However, aside from these cost-sharing methods, there are three other things to know about Part D drug plans:

- Drug Tiers

- Part D stages

- Part D IRMAA brackets

There are also late enrollment penalties, which I’ll discuss more in the enrollment section.

Now let’s take a closer look at these 3 things.

What Are Part D Drug Tiers?

Instead of setting different copays for every drug in their formulary, Most Part D drug plans group their drugs into tiers. Low tiers like Tier 1 usually include generic drugs and typically have low or no cost-sharing. Higher tiers like Tier 3 – 6 may include non-preferred brand-name drugs, and will usually have higher cost-sharing methods for you.

Each plan provider is free to set their own tiers. Some have only three tiers, while other plans have as many as six tiers.

To give you an idea of what these tiers look like, here’s how one plan in Los Angeles set their tiers back in 2024:

| Tier: | Cost Sharing: |

| Tier 1: Preferred generic drugs | $1 copay |

| Tier 2: Non-preferred generic drugs | $10 copay |

| Tier 3: Preferred brand-name drugs | $47 copay |

| Tier 4: Non-preferred brand-name drugs | 45% coinsurance |

Again, the tiers above are just an example, each Part D plan will have its own set of tiers. However, most plans will have something similar to this.

Also, tiers are only applicable during the Initial Coverage Stage. Which leads us to the next things to know about Part D costs:

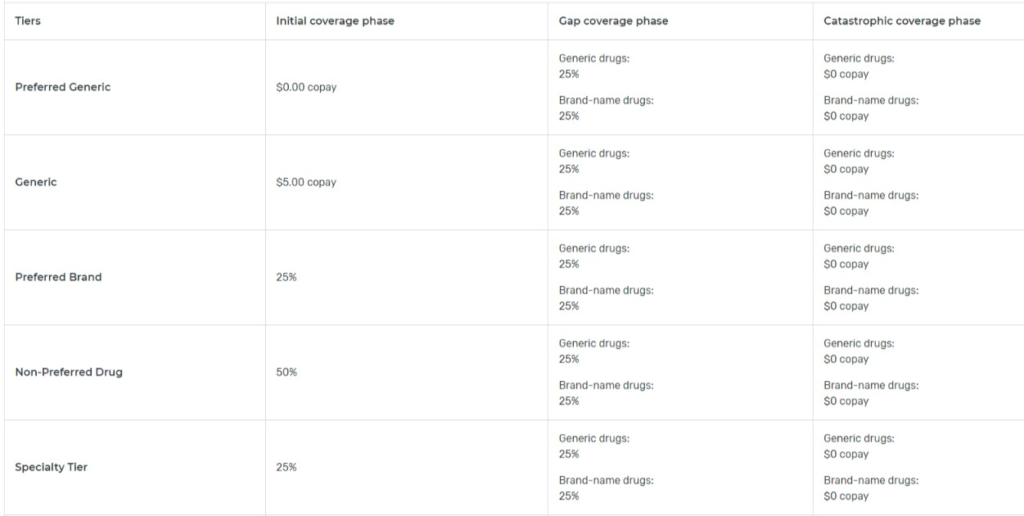

What Are The Stages of Medicare Part D?

There are 3 payment stages for Medicare Part D in 2026: the Deductible Stage, the Initial Coverage Stage, and the Catastrophic Coverage Stage.

The biggest change already happened in 2025: the Coverage Gap, often called the Donut Hole, was removed. In 2026, that simpler 3-stage structure is continuing, but the dollar amounts changed slightly.

But for now, here’s how it works in 2026:

- Deductible Stage – In this stage, you may pay 100% of your drug costs until you reach your plan’s deductible. Plans can set their own deductibles, but in 2026, the maximum Part D deductible is $615. Once you’ve met your deductible, you move to the Initial Coverage Stage. If your plan has no deductible, you move straight to the Initial Coverage Stage.

- Initial Coverage Stage – In this stage, your Part D plan starts helping cover your medications. With the standard Part D benefit, you generally pay 25% of covered drug costs in this stage, though actual plan costs can vary depending on your drug tier, pharmacy, and plan design. This stage lasts until you reach $2,100 in out-of-pocket costs for covered Part D drugs.

- Catastrophic Coverage Stage – Once you reach the $2,100 out-of-pocket limit, you move into Catastrophic Coverage. In 2026, you pay $0 for covered Part D drugs for the rest of the year.

That means the old Donut Hole explanation no longer applies in 2026. Instead of moving into a Coverage Gap after a certain amount of total drug costs, your main number to watch is the $2,100 out-of-pocket limit.

Keep in mind that these stages reset every January 1.

What Are Part D IRMAA Brackets?

If you are someone in a higher income bracket, you have to pay an additional fee on top of your Part D premium. This is calculated using your Modified Adjusted Gross Income (MAGI) from 2 years prior.

| Individual Tax Return | Joint Tax Return | Married & Separated Tax Return | Additional fee |

| $109,000 & below | $218,000 & below | $109,000 & below | $0 |

| $109,001 – $137,000 | $218,001 – $274,000 | N/A | + $14.50 |

| $137,001 – $171,000 | $274,001 – $342,000 | N/A | + $37.50 |

| $171,001 – $205,000 | $342,001 – $410,000 | N/A | + $60.40 |

| $205,001 – $499,999 | $410,001 – $749,999 | $109,001 – $390,999 | + $83.30 |

| $500,000 & above | $750,000 & above | $391,000 & above | + $91.00 |

If your income is significantly lower now than it was 2 years ago, you can appeal your IRMAA bracket to the SSA.

Enrolling in Medicare Part D

Now that you know what Part D is, and how much it could cost, let’s move on to enrolling in Part D!

When Can You Enroll in Medicare Part D?

You can typically enroll in Medicare Part D when you first become eligible for Medicare. This is the same 7-month Initial Enrollment Period (IEP) as Original Medicare. It starts 3 months before your 65th birth month and ends 3 months after your 65th birth month.

If your birthday is the 1st day of a month, your IEP will start 4 months before your birth month, and end 2 months after it.

Remember, you enroll in a Part D plan separately from Parts A and B. Some people make the mistake of thinking Part D is included in Original Medicare, but it’s not.

Also, you will need to be enrolled in either Part A or B to be eligible for Part D, so do that before enrolling in Part D (you’ll also need both Parts A and B to be eligible for an Advantage Plan with Part D included).

It’s a good idea to enroll in a Part D drug plan during the Initial Enrollment Period, if it sounds like the right plan for you, even if you aren’t taking prescription medications yet. This is because if you enroll late, you’ll get permanent late enrollment penalties.

Note: if you miss your Initial Enrollment Period, you can enroll in a Part D plan during the Fall Open Enrollment Period (Oct 15 – Dec 7), which happens every year.

What Are the Part D Late Enrollment Penalties?

If you don’t enroll in Part D during the Initial Enrollment Period – and you go without creditable drug coverage for 63 days – you’ll get a permanent penalty on your Part D premiums.

This is an additional 1% to your premium for every month you delay enrolling in Part D and don’t have creditable drug coverage.

Creditable drug coverage means a drug plan that’s equal to or better than Medicare Part D. If you have a drug plan under your employer, VA benefits, TRICARE, or other institutions, you can ask them if their drug coverage is creditable.

If it is, then you can delay Part D coverage without incurring penalties.

Once your creditable drug coverage ends, you’ll have a Special Enrollment Period (SEP) of 62 days to enroll in Medicare Part D. If you don’t enroll within this SEP, you’ll start getting permanent penalties.

Now let’s take a look at an example situation:

- 65th Birthday: July 20, 2026

- IEP: April 1 – October 31, 2026

- Creditable Coverage: None

- Enrolls in Part D: October 15, 2027

- Penalty: 11 months late = 11% penalty

- Part D Average Premium: $34.50/month

- Premium With Penalty: $38.29/month ($34.50 + 11%)

Let’s say your 65th birthday is on July 20. This means your Initial Enrollment Period (IEP) will run from April 1 to October 31. And say you don’t enroll during your IEP, and you don’t have creditable drug coverage.

The next year, you decide to enroll in a Part D plan. But since your IEP is over, you typically must wait for the Fall Open Enrollment Period (Oct 15 – Dec 7) to enroll. You finally get a Part D plan on October 15.

Since your IEP ended in November, and you enrolled in October, that’s 11 months without creditable drug coverage. This means you’ll get an 11% penalty on your Part D premium.

Remember, the penalty is permanent! You’ll be paying this penalty for as long as you have Part D (essentially for the rest of your life).

That’s why I recommend enrolling as soon as you become eligible!

You might not need prescription medication coverage now. But a few years later if you do, you may be glad you enrolled in time.

How to Find Part D Drug Plans in Your Area

To find Part D plans in your area, you can call a plan provider, call Medicare, ask for help from a professional broker, or find plans using Medicare’s plan finder tool.

Remember, Part D plans are localized. This means that the plans available to you will depend on where you live.

That’s why before enrolling, shop for the plans that are available in your area.

To find plans, I don’t recommend going straight to an insurance company. You can tell them what your needs are, but in the end, they’re only going to sell you their plans.

Instead, you can talk to an independent Medicare broker.

Independent Medicare brokers have contracts with many insurance companies in your area. This way, they can listen to your needs, and recommend a plan that’ll work best for you.

The best part?

Medicare brokers are paid by commission, so you won’t have to pay anything to get their help.

But if you want to find a plan by yourself, you can use Medicare’s Plan Finder Tool.

To use this, simply enter your ZIP code, select Part D, answer a few questions, and then you’ll get a full list of Part D plans available in your area.

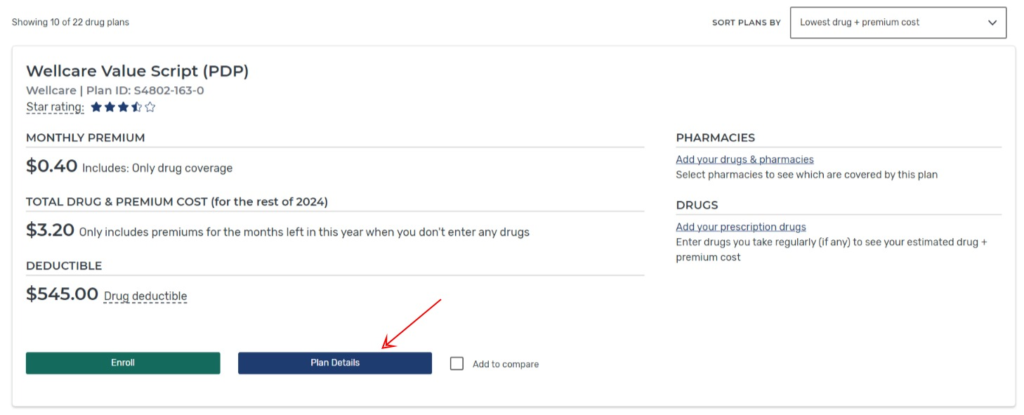

If you find a plan you’re interested in, you can click on “Plan Details” to learn more.

This will show you the cost-sharing terms of the plan. However, this will not show you the plan’s formulary.Visit the plan’s website to find this.

If you like the plan, you can click on the “Enroll” button to start the enrollment process!

When searching for plans, you can also include the prescription medicines you take and your preferred pharmacies. This’ll filter out search results that don’t fit the criteria, and make it a lot easier for you to find the right plan.

Can You Switch Your Part D Drug Plan?

Yes, you can switch your Medicare Part D plan during the Fall Open Enrollment Period, which runs from October 15 to December 7 every year.

Every year, Medicare Part D plans can change their terms.

Your plan provider should send you a summary of these changes before the Open Enrollment Period. Review these changes regularly because sometimes they stop covering your drugs, or your preferred pharmacy might not be included in their network anymore.

After reviewing these changes, shop around for better options (even if you’re okay with the changes). This is because there may be a new plan that fits your needs more closely than your current one.

Then from October 15 to December 7, you’re free to enroll in a new plan.

Aside from the Open Enrollment Period, you can get a Special Enrollment Period (SEP) for several reasons. For example, if you move somewhere outside your current plan’s coverage area, Medicare will typically give you a 3-month SEP to get a new Part D plan.

You can find the full list of SEPs for Part D on Medicare’s website.

How to Save On Medicare Part D

Aside from enrolling on time to avoid penalties, and comparing plans to find the one with the lowest costs for what you need, there are several ways you can save on your prescription meds.

This is especially true for people who are in lower income brackets.

Three main ways to save on Part D are:

- Enrolling in Extra Help

- Checking if your state has a pharmaceutical assistance plan

- Checking if your drug manufacturer has an assistance program

Extra Help is Medicare’s assistance program for Part D. With it, you typically won’t have to pay your Part D premium and deductible.

Instead of your plan’s copays and coinsurances, you could have a fixed $4.50 copay for generic drugs and a $11.20 copay for brand-name drugs.

If you’re enrolled in Extra Help, you also don’t have to worry about the Part D late enrollment penalty.

You’ll typically get Extra Help automatically if you:

- Are enrolled in a Medicare Savings Program (MSP)

- Have full Medicaid coverage

- Are getting Supplemental Security Income from Social Security

If none of these apply to you, you can generally enroll in Extra Help if you meet the financial requirements:

| Individuals | Couples | |

| Annual Income Limits | $23,940 | $32,460 |

| Resource Limits | $18,090 | $36,100 |

Some states also have pharmaceutical assistance programs that could help you pay for your prescription medications.

Each state has its own set of requirements on who can enroll in these plans.

To see if your state has an assistance program, Medicare has a tool on its website that helps you find these.

Finally, some drug manufacturers help pay for the costs of their medications.

If you’re taking a specific drug, you can check if there are manufacturer discounts on Medicare’s website.

Conclusion: Ready to Enroll in a Medicare Part D Plan?

And that’s Medicare Part D!

Yes, it’s definitely one of the most confusing parts of Medicare.

But Part D is a huge help for people who need a lot of medications. Sadly, a lot of people don’t use it to its full potential.

That’s exactly why I wrote this article!

I hope that by reading this, you know how to save a lot of money in the long run. And I hope that you’re now ready and confident to enroll in a Part D plan if it’s the right plan fit for you.

If you have any questions, don’t hesitate to reach out.

Or, if you need professional help finding and comparing plans in your area, you can contact +1 877-360-6565 (TTY: 711), to talk to my team of licensed insurance agents today:

Calvin Bagley is the founder of PlanFit, The Medicare Store, and Nuvo Health. He and his team have helped over 60,000 people navigate Medicare options, and he’s a nationally recognized speaker in the Medicare industry. Most importantly, he’s someone who believes every American deserves clear, honest information without pressure.