According to Forbes.com, 65% of people enrolled in Medicare find the program difficult to understand.

Yep. Who’s surprised.

With so many terms, acronyms, enrollment periods, and payment schemes, of course people have a ton of questions about Medicare—especially people who are about to turn 65.

To make matters worse, if you make mistakes with Medicare, you can end up with permanent Medicare penalties or find yourself “stuck” in a plan that isn’t the right fit for you.

That’s why we’re answering 21 of the top Medicare questions. We divided these questions into four categories:

- Getting Started with Medicare

- Costs and Penalties

- Medicare Coverage, and

- Finding the Plan Fit For You

By the end, you’ll find Medicare much easier to manage.

Getting Started With Medicare

#1: What Is Medicare?

Medicare is a health insurance program primarily designed for Americans aged 65 and above. It typically consists of Medicare Part A (hospital insurance), and Medicare Part B (medical insurance).

Together, Medicare Part A and B are known as Original Medicare, and are provided by the federal government. There are other optional parts of Medicare provided by licensed insurance companies, which we will talk more about below.

#2: Who is Eligible For Medicare?

All citizens of the United States who are aged 65 or older can enroll in Medicare. Medicare is also available for certain people with disabilities (must be receiving Social Security disability benefits for at least 24 months), end-stage renal disease (ESRD), or ALS (Lou Gerig’s disease).

#3: What’s the Difference Between Medicare and Medicaid?

Medicare is a health insurance program primarily designed for Americans aged 65 or older. Medicaid is a state and federal health program that assists people in lower income brackets.

Each state has its own requirements for enrolling in Medicaid. However, if you qualify for both Medicare and Medicaid, you can enroll in both programs.

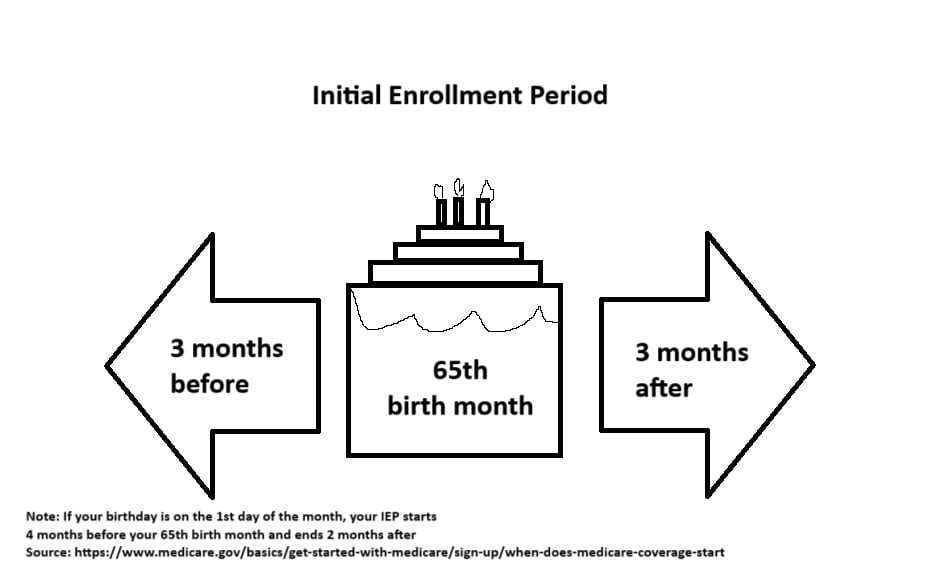

#4: When Can You Enroll in Medicare?

Most people can enroll in Medicare during their Initial Enrollment Period. This is a seven-month window that starts three months before your 65th birth month, and ends three months after your 65th birth month.

If your birthday falls on the first day of the month, your Initial Enrollment Period starts four months before your 65th birth month, and ends two months after your 65th birth month.

You can also typically enroll in Medicare before you turn 65 if you have been taking Social Security disability benefits for 24 months, or if you have ESRD or ALS.

#5: Will You Automatically be Enrolled in Medicare When You Turn 65?

If you have been receiving Social Security benefits for at least four months before turning 65, you will automatically be enrolled in Medicare once you turn 65.

However, if you are not yet receiving Social Security benefits, you may have to enroll manually once your Initial Enrollment Period begins.

Note: It’s a good practice to confirm with Social Security whether you’ve been automatically enrolled in Medicare once you turn 65. There are some cases where someone should’ve been automatically enrolled, but was not.

#6: Is Medicare Mandatory?

No, it is not mandatory to enroll in Medicare.

However, if you don’t enroll in Medicare when you turn 65, and you don’t have creditable coverage from elsewhere (such as an employer group plan), you may be subject to permanent late enrollment penalties once you decide to enroll in Medicare.

#7: What Can You Do If You Can’t Afford Medicare?

There are several state-run programs that help you lower your costs with Medicare. To find out if you are eligible for these programs, visit Medicare’s website.

Section Quiz

Question: True or false? You must enroll in Medicare once you turn 65 otherwise, you will incur late enrollment penalties.

- Typically False. If you have creditable health coverage from elsewhere, such as an employer’s group coverage, you may be able to delay enrolling in Medicare without incurring penalties. You can contact your current health insurance plan to find out if your plan is considered “creditable” or not.

Question: True or false? If your 65th birthday is on February 1, 2026, your Initial Enrollment Period starts on October 1, 2025 and ends on April 30, 2026.

- Typically True. Most people’s Initial Enrollment Period starts three months before their 65th birth month and ends three months after. However, if your birthday falls on the first day of the month, your Initial Enrollment Period starts four months before your 65th birth month and ends two months after.

Question: True or false? If you enroll in Medicare, you no longer qualify for Medicaid (and vice versa).

- Typically False. Generally speaking, if you qualify for Medicare and your state’s Medicaid program, you may enroll in both.

Question: If you are not receiving Social Security benefits yet, it’s your responsibility to enroll in Medicare when you become eligible to avoid late enrollment penalties.

- Typically True. If you are not receiving Social Security or Railroad Retirement Board benefits, you won’t normally be automatically enrolled in Medicare. Most people also don’t receive reminders that it is their Initial Enrollment Period since you are responsible for knowing when to enroll to avoid penalties.

Costs and Penalties

#8: How Much Does Medicare Cost?

Your Medicare costs depend on the parts and plans that you enroll in.

Medicare Part A has a $0 premium for most people. As long as you’ve worked and paid Medicare taxes for 40 or more quarters (10 years), you won’t have to pay premiums for Medicare Part A.

Medicare Part B usually has a base premium of $202.90/month in 2026. However, if you are in a higher income bracket, you may have to pay more for Medicare Part B.

Aside from premiums, both Medicare Part A and B have cost-sharing schemes. You’re also responsible for paying deductibles, copays, or coinsurance whenever you get covered services (more on this below).

#9: What is Medicare IRMAA?

Medicare’s Income-Related Monthly Adjusted Amount (IRMAA) is a surcharge given to people in higher income brackets. If you are in a higher IRMAA bracket, you’ll typically have to pay higher premiums for Medicare Part B.

Here’s a quick look at the IRMAA brackets for 2026:

| 2025 IRMAA Brackets | |||

| Individual Tax Return | Joint Tax Return | Married & Separated Tax Return | Part B Premium |

| 109,000 & below | $218,000 & below | $109,000 & below | $202.90 |

| $109,001 – $137,000 | $218,001 – $274,000 | N/A | $284.10 |

| $137,001 – $171,000 | $274,001 – $342,000 | N/A | $405.80 |

| $171,001 – $205,000 | $342,001 – $410,000 | N/A | $527.50 |

| $205,001 – $499,999 | $410,001 – $749,999 | $109,001 – $390,999 | $649.20 |

| $500,000 & above | $750,000 & above | $391,000 & above | $689.90 |

Note: your Medicare IRMAA is calculated by taking your MAGI number from your tax return two years prior.

If you are earning less today than you were two years prior because of a “life-changing” event, you can contest your IRMAA bracket. “Life-changing” events include marriage, divorce, death of a spouse, work reduction, retirement, loss of income-producing property, loss of pension income, and employer settlement payments.

#10: What Will My Out-of-Pocket Costs Look Like With Medicare?

Both Medicare Part A and B have deductibles, copays, and coinsurance that you’re responsible for paying out-of-pocket.

Here’s a quick overview of the costs in 2025:

| Item | 2025 Cost |

| Medicare Part A Premium | $0 for most people |

| Medicare Part A Deductible | $1,736 |

| Inpatient hospital stay copays | Day 1 – 60 = $0 Day 61 – 90 = $434/day Day 91 – 150 = $868/day using lifetime reserve days* Day 150+ = you pay 100% |

| Skilled nursing facilities | Day 1 – 20 = $0 Day 20 – 100 = $217/day Day 100+ = you pay 100% |

| Hospice care | $0 for covered services 5% for in-patient respite care $5 copay for prescription drugs |

| Item | 2025 Cost |

| Medicare Part B Premium | $202.90/month (base premium) |

| Medicare Part B Deductible | $283 |

| General costsAt-home medical equipmentMental health diagnosis/treatmentPartial hospitalization mental health careOutpatient hospital care | 20% coinsurance for Medicare-approved amount |

| Clinical laboratory servicesCovered home healthcareYearly depression screeningOther preventive and screening measures | $0 |

Note: There is no limit on your out-of-pocket expenses with Original Medicare. This is why many people who enroll in Medicare also get additional coverage in the form of Medicare Advantage Plans or Medicare Supplement Plans—which both typically cap your out-of-pocket spending every year to a certain amount.

#11: How Much is the Medicare Part B Late Enrollment Penalty?

If you miss your Initial Enrollment Period and don’t have creditable coverage, you might have to pay a late enrollment penalty for Medicare Part B.

The late enrollment penalty is an extra 10% added to your Medicare Part B premium for every year you delay enrolling without creditable coverage.

Section Quiz

True or False? Medicare Part A is free for everybody.

- False. Medicare Part A typically has a $0 premium for most people. However, if you haven’t paid Medicare taxes for 40 or more quarters, you should have a premium for Medicare Part A.

True or False? In 2026, if you made over $106,000/year at age 63 before you retired and decide to retire at 65, now making less than $106,000/year, you can contest your IRMAA bracket and won’t have to pay the surcharge.

- Typically True. Medicare IRMAA is calculated using the MAGI number from your tax return two years prior. If you have had a life-changing event since then, such as retirement, you can contest your IRMAA bracket and have your surcharge removed.

True or False? Original Medicare has an out-of-pocket limit.

- False. Original Medicare has no out-of-pocket limit, which is one of the main reasons why most people opt to enroll in additional coverage. Without additional coverage, you may be at risk of high out-of-pocket expenses.

True or False? In 2026, you must spend $283 out-of-pocket on Medicare Part B covered services first before Medicare Part B starts covering you.

- Typically True. This is known as a deductible. Medicare Part A also has a deductible, which is set to $1,736 in 2026.

Medicare Coverage

#12: What Are Your Medicare Coverage Options?

There are generally five parts and plans for Medicare:

- Medicare Part A – Hospital insurance part of Original Medicare

- Medicare Part B – Medical insurance part of Original Medicare

- Medicare Supplement Plans – Private insurance that acts as secondary insurance to Original Medicare. Medicare Supplement Plans help cover your out-of-pocket expenses in Original Medicare. There are ten standardized Medicare Supplement Plans available today, namely Medicare Supplement Plan (Medigap) A, B, C, D, F, G, K, L, M, and N.

- Medicare Part D – Prescription drug plans. Medicare Part D plans are provided by private insurance companies working closely with Medicare. You can enroll in either a standalone Medicare Part D plan or a Medicare Advantage Plan with built-in Medicare Part D coverage.

- Medicare Part C (Medicare Advantage Plans) – Medicare Advantage Plans are provided by private insurance companies. When you enroll in a Medicare Advantage Plan, Medicare pays your insurance company a set amount and transfers responsibility of your healthcare to your insurance company. Medicare Advantage Plans are required to cover everything included in Medicare Parts A and B. Most Medicare Advantage Plans also have built-in Medicare Part D prescription drug coverage. Many also have benefits for dental, vision, and hearing care, as well as many other perks. Because of the way they work, many Medicare Advantage Plans have a $0 premium.

#13: Does Medicare Cover Prescription Drugs?

Original Medicare does not cover most commercially available prescription drugs sold in pharmacies.

However, you could enroll in a Medicare Part D prescription drug plan. You can do this by enrolling in a standalone Medicare Part D plan or a Medicare Advantage Plan with a built-in prescription drug plan.

#14: Does Medicare Cover Routine Dental Care?

Original Medicare typically doesn’t cover routine dental care like teeth cleaning, extractions, root canals, and other dental procedures.

However, many Medicare Advantage Plans have some benefits for dental coverage.

#15: Does Medicare Cover Routine Eye Care?

Original Medicare typically doesn’t cover routine eye care. Original Medicare usually covers eye disease treatment or surgery (such as glaucoma or macular eye degeneration). However, routine eye care like eye exams or eyeglasses is generally not covered by Original Medicare.

Some Medicare Advantage Plans have coverage for routine eye care.

#16: Does Medicare Cover Hearing Aids?

Generally no. Original Medicare does not usually cover hearing aids. However, some Medicare Advantage Plans may have coverage for hearing aids. If you enroll in a Medicare Advantage Plan, be sure to check the plan’s perks to find out if it covers hearing aids.

#17: Does Medicare Cover You While Traveling?

Travel coverage with Medicare depends on the type of plan that you have. If enrolled in Original Medicare only, you should be covered in any hospital or doctor around the United States and territories that accept Medicare. However, Original Medicare doesn’t cover healthcare expenses outside the United States and territories.

Medicare Supplement Plans also should cover you for any doctor or hospital that accepts Medicare. Some of these plans (namely Medicare Supplement Plan C, D, F, G, M, and N) also cover 80% of your foreign travel emergency costs, with a $50,000 lifetime limit.

Medicare Advantage Plans generally have local networks of doctors and hospitals that they cover. If you enroll in a Medicare Advantage Plan with a local network, you may have limited options if you travel outside your city or county. However, Medicare Advantage Plans should cover you for emergencies, even if you go out-of-network. Some Medicare Advantage Plans also have coverage for foreign travel emergencies.

Section Quiz

True or False? If you enroll in Original Medicare and a Medicare Supplement Plan, you should have coverage for most prescription drugs.

- Typically False. Original Medicare and Medicare Supplement Plans don’t cover most prescription drugs. Many people who choose to enroll in a Medicare Supplement Plan also enroll in a standalone Medicare Part D prescription drug plan to have their drugs covered.

True or False? Medicare Advantage Plans with $0 premiums are legitimate Medicare plans.

- True. Because Medicare pays your insurance company a fixed amount when you enroll in their Medicare Advantage Plans, many Medicare Advantage Plans can have a $0 premium without compromising their health coverage.

True or False? If you enroll in Original Medicare, a Medicare Supplement Plan, and a Medicare Part D prescription drug plan, you’ll be covered for all routine dental, vision, and hearing care.

- False. Original Medicare does not cover most routine dental, vision, and hearing care services. Medicare Supplement Plans are secondary insurance to Original Medicare, so they typically don’t have additional coverage to Original Medicare. That’s why you may have to purchase separate insurance for routine dental, vision, and hearing care or pay out-of-pocket.

True or False? If you have a medical emergency and go to a hospital outside of your Medicare Advantage Plan’s network, your Medicare Advantage Plan should cover your costs.

- Typically True. If you get services outside of your Medicare Advantage Plan’s network, you may not be covered, or you may have to pay higher copays. However, during an emergency, your Medicare Advantage Plan should cover your out-of-network costs.

Finding the Right Plan Fit For You

#18: What’s the Most Popular Medicare Supplement Plan?

The most common Medicare Supplement Plans are Medicare Supplement Plan F, G, and N.

Medicare Supplement Plan F covers all the gaps in Original Medicare, which means you shouldn’t have any out-of-pocket expenses if you enroll in a Medicare Supplement Plan F.

However, Medicare Supplement Plan F is no longer available for people who turn 65 on or after January 1, 2020.

Medicare Supplement Plan G covers most gaps in Original Medicare except the Medicare Part B deductible (which is set to $283 in 2026). However, Medicare Supplement Plan G typically has higher premiums than other plans.

Medicare Supplement Plan N doesn’t cover the Medicare Part B deductible and Medicare Part B excess charges, it also has copays for when you visit the doctor or ER. However, Medicare Supplement Plan N generally has lower premiums than Medicare Supplement Plan G.

The other seven Medicare Supplement Plans have significantly lower enrollment numbers than Medicare Supplement Plan F, G, and N.

#19: What’s the Difference Between an HMO and a PPO Medicare Advantage Plan?

HMO (Health Maintenance Organization) Medicare Advantage Plans usually don’t cover you outside of their network unless it is an emergency.

In contrast, PPO (Paid Provider Organization) Medicare Advantage Plans could cover you for out-of-network services, but you may have to pay higher copays.

There are several other differences, including costs, benefits, primary care physicians, and claims filing. Here’s a quick summary of the differences between HMO and PPO Medicare Advantage Plans:

| HMO | PPO | |

| 1. Out-of-Network Coverage | Typically doesn’t cover you for out-of-network services (except in emergencies) | Typically has higher copays and higher out-of-pocket maximums for out-of-network services |

| 2. Costs | Typically costs less than PPOs | Typically costs more than HMOs |

| 3. Benefits | Usually more benefits than PPOs | Usually less benefits than HMOs |

| 4. Primary Care Physicians | Usually have to choose a primary care physician May need referrals to see specialists | Usually don’t need a primary care physician Usually don’t need referrals to see specialists |

| 5. Claims Filing | No need to file claims in-network | No need to file claims in-network You may need to pay up-front for out-of-network services and then request reimbursement from your plan |

#20: Which Is Better? Medicare Supplement Plans or Medicare Advantage Plans?

Neither Medicare Supplement Plans or Medicare Advantage Plans are better or worse than the other. It depends on your lifestyle, budget, and the plans available in your area.

Below is a comparison chart to help you get a better idea of the differences between these two plan types:

| Medicare Advantage Plans | Medicare Supplement Plans | |

| Covers | Everything in Original Medicare (Part A and B) Prescription drug coverage (most plans) Dental, vision, and hearing care (some plans) Other perks | Most of the out-of-pocket expenses in Original Medicare (Part A and B) |

| Plan Options | HMO PPO PFFS SNP MSA | Ten standardized plans: Medigap Plan A, B, C, D, F, G, K, L, M, and N |

| Cost | $0 – $200+/month (Average $18.5/month according to the KFF) Deductibles and copays (vary by plan) Maximum out-of-pocket (varies by plan) | Depends on plan type, location, age, and other factors Plan G: roughly $100 – $300/month* Plan N: roughly $70 – 270/month* |

| Doctors and Hospitals | Typically has networks of local doctors and hospitals May require referrals or prior authorizations for special treatment | Any doctor or hospital that accepts Medicare Typically doesn’t require referrals or prior authorizations |

| Annual Changes | Plans typically change terms every year | Coverage usually doesn’t change, but prices may increase every year |

| Enrollment Periods | Initial Enrollment Period (IEP) Annual Election Period (AEP) Medicare Advantage Open Enrollment Period (MA OEP) Special Enrollment Periods (SEPs) No medical underwriting | Medigap Open Enrollment Period (OEP) Special Enrollment Periods (SEPs) May require medical underwriting if you enroll outside your Medigap OEP or a SEP |

*These are rough estimates. Price range varies by age, location, and other factors. To find accurate price ranges, chat with a licensed insurance agent at no cost to you.

#21: Are Medicare Advantage Plans Bad?

No. While Medicare Advantage Plans may have some things certain people don’t enjoy, some people online exaggerate these issues to make Medicare Advantage Plans seem “bad.”

People who do this are often sales agents for Medicare Supplement Plans (or people who listen to them).

In reality, both Medicare Advantage Plans and Medicare Supplement Plans have their pros and cons. The “better” plan is going to be different for everyone.

That’s why when you see someone who is clearly biased against Medicare Advantage Plans (which happens often online), it should be a warning to you that this person may not have your best interest in mind.

Section Quiz

True or False? Medicare Supplement Plan G is generally more expensive than other Medicare plans.

- True. Medicare Supplement Plan G covers most of the gaps in Original Medicare. However, one of the downsides of Medicare Supplement Plan G is that it can be expensive for many people.

True or False? If enrolled in a Medicare Advantage PPO plan, you won’t receive coverage when you get services outside your plan’s network.

- Typically False. Medicare Advantage PPO plans typically cover you out-of-network, but you may have to pay higher copays. Meanwhile, Medicare Advantage HMO plans typically don’t cover you out-of-network unless it’s an emergency.

True or False? If an agent is heavily biased towards one plan type, you should be careful about dealing with them.

- True. Both Medicare Supplement Plans and Medicare Advantage Plans have pros and cons. A licensed insurance agent should listen to your needs, help you understand each plan type, and guide you to the right plan fit for you. Agents who are strongly against one plan or the other may have ulterior motives.

Where Can You Get Unbiased Help Comparing Your Medicare Options?

If you’re looking for unbiased help, you can contact a licensed insurance agent. Licensed insurance agents contract with several different companies, and can listen to your specific needs and help you find the right plan fit for you.

When choosing an agent, it’s a good idea to ask whether they sell both Medicare Supplement and Medicare Advantage Plans. Asking this ensures that your agent is unbiased.

Our licensed insurance agents here at PlanFit are paid a salary, not commissions. This allows us to provide you with completely unbiased opinions since they are paid the same regardless of which plan you enroll in.

Not only that, but you can get our services at no cost to you.

So if you’re looking for unbiased help finding the right Medicare plan fit for you, call or text our team of licensed insurance agents at +1 877-360-6565 (TTY: 711) and we’d be glad to assist you.

Alternatively, you can watch our Medicare Made Simple workshop if you’d iike to go deeper:

Calvin Bagley is the founder of PlanFit, The Medicare Store, and Nuvo Health. He and his team have helped over 60,000 people navigate Medicare options, and he’s a nationally recognized speaker in the Medicare industry. Most importantly, he’s someone who believes every American deserves clear, honest information without pressure.