There are hundreds of Medicare horror stories out there.

You hear stories of hospitals denying people coverage and stories of huge penalties that people have to pay for the rest of their lives.

And the worst part?

Many of these stories are real, and some could even happen to you.

That’s why it’s so important to be aware of all the potential landmines of Medicare.

In this article, we’ll go over the 15 worst Medicare mistakes you can make and how to avoid them.

When you know these, you can enroll in Medicare and get the coverage you need without spending a dime extra!

Mistake #15: Assuming Medicare is Free

Medicare is NOT free!

This one catches a lot of people off guard.

They enroll in Medicare thinking it’s a free government program, then get shocked when $174.70 is taken off their Social Security check for their “Medicare Part B premium.”

Not only is Medicare not free, but it doesn’t cover all your healthcare expenses either.

There are also deductibles, copays, and coinsurances that you have to pay out-of-pocket whenever you visit a hospital or a doctor’s office.

Will Medicare drastically reduce your healthcare costs?

Typically, yes.

But is it free?

A big no.

How to Avoid This Mistake

Educate yourself.

It’s something everyone turning 65 needs to do.

A good place to start is our workshop, which will teach you all the basics of Medicare (including all the costs and how to avoid penalties).

But in a nutshell, here’s what you need to pay:

- Premium: The amount you have to pay every month to keep your Medicare coverage active. Most people don’t have to pay a premium for Medicare Part A (inpatient and hospital coverage), but in 2026 there’s a $202.90/month premium for Medicare Part B (outpatient coverage).

- Deductibles: The amount you have to pay out-of-pocket before Medicare starts covering you. In 2026, it’s $1,736 for Medicare Part A and $283 for Medicare Part B.

- Copay: A cost-sharing method where you pay a fixed amount, and Medicare covers the remaining cost. For example, if you’re admitted to a hospital for over 60 days, you’ll have to make a $434 copayment for every additional day up to 90 days. After that, it gets even more expensive!

- Coinsurance: A cost-sharing method where you pay a percentage of the total cost. For example, most Medicare Part B services and items come with a 20% coinsurance. If you visit your doctor’s office and the cost is $100, you’ll pay $20 and Medicare will cover the remaining $80.

That’s just the basics.

Be sure to view our Medicare Workshop for more information. You can also visit our YouTube channel to learn about all things Medicare!

Mistake #14: Assuming You Don’t Need to Enroll in Medicare

If you’re covered by COBRA, a retiree plan, or some other health insurance, you might assume you don’t need Medicare when you turn 65.

After all, you’re happy with the health coverage, so you can skip Medicare for now.

Big mistake!

Unless you’re in your (or your spouse’s) company health insurance plan, and that company has 20 or more employees, you need to enroll in Medicare when you turn 65.

You may be happy with your coverage now, but when you turn 65, it could get change significantly.

This is because, most of the time when you turn 65 and don’t have creditable coverage, Medicare automatically becomes the first payer for your healthcare. Your current healthcare plan will become the second payer.

That’s why it’s so important to check if you have creditable coverage when you turn 65.

If you don’t have creditable coverage, and delay enrolling in Medicare, you may also incur late enrollment penalties (which we’ll get more into later).

Mistake #13: Assuming You MUST Enroll in Medicare When You Turn 65

Some people make the opposite mistake and think they have to enroll in Medicare when they turn 65.

While it’s usually a popular option, enrolling in Medicare blindly might not be the right decision for many people.

If you have creditable coverage from your employer (as always, with 20 or more employees), there are several reasons you may want to delay.

One reason is if your employer’s plan also covers your spouse.

If you decide to switch to Medicare and cancel your work insurance, your spouse will lose their coverage.

The same goes if your employer’s plan covers your children. Medicare only covers you, so your kids won’t have coverage if you switch and cancel your work coverage.

It also doesn’t make a lot of sense to keep both your employer plan and Medicare.

Remember, Medicare is not free!

You’ll be paying for two plans, and the benefits will overlap so much that it might not be worth it.

How to Avoid This Mistake

Before turning 65, study your employer’s plan closely and compare it with Medicare.

If there’s one thing to know by now, it’s not to make assumptions about Medicare.

Look at the specific details of both plans to determine which is a better fit for you!

Mistake #12: Not Paying Your Premiums

We know that, for some people, spending $202.90 every month is painful – especially if they don’t need healthcare coverage yet.

Maybe the Medicare premiums were okay when you first turned 65, but now that you stopped working, you may feel like you could really use the extra money.

If you find yourself in this situation, you may want to wait before you just stop paying your premiums!

Remember, the premium might be expensive now, but have you seen how much hospitals and doctors charge?

If you get sick, you’ll be relieved you have Medicare coverage.

If you’re struggling to pay your premiums, Medicare has several programs to assist you.

These are called Medicare Savings Programs, or MSPs. If you qualify, these programs could help cover your Medicare premiums for you.

There are also a lot of other assistance programs out there, such as Extra Help for drug coverage and others.

How to Avoid This Mistake

Always remember that the premiums are only a fraction of what your healthcare bill can cost you.

It’s also a good idea to familiarize yourself with Medicare’s assistance programs.

A good place to start is to read Medicare’s articles on Medicare Savings Programs, Medicaid, and Extra Help.

This way, if you really can’t afford to pay your premiums anymore, you can turn to one of these.

Mistake #11: Not Contesting Your IRMAA Bracket

In case you didn’t know, people who earn more typically pay more for Medicare.

Medicare has something called IRMAA brackets (income-related monthly adjustment amounts) that adjust your premium based on your Monthly Adjusted Gross Income.

Here are the IRMAA brackets for 2024:

| Individual Tax Return | Joint Tax Return | Married & Separated Tax Return | Additional fee (total monthly premium) |

| $103,000 & below | $206,000 & below | $103,000 & below | $0 ($174.7) |

| $103,001 – $129,000 | $206,001 – $258,000 | N/A | + $69.9 ($244.6) |

| $129,001 – $161,000 | $258,001 – $322,000 | N/A | + $174.7 ($349.4) |

| $161,001 – $193,000 | $322,001 – $386,000 | N/A | + $279.5 ($454.2) |

| $193,001 – $499,999 | $386,001 – $749,999 | $103,001 – $396,999 | + $384.3 ($559) |

| $500,000 & above | $750,000 & above | $397,000 & above | + $419.3 ($594) |

But be careful.

It takes these numbers from your tax return from 2 YEARS ago.

This means that if you earned over $103,000 when you were 63 and still working, you’d be charged for the second bracket – even if you’re already 65, retired, and earning less than $103,000 a year!

And the worst part?

A lot of people who could contest their IRMAA bracket, don’t. They just pay the extra $69.90/month, which adds up to an extra $838.80/year that they may not even have to pay.

How to Avoid This Mistake

The good news is that you can contest your IRMAA bracket.

Medicare says that you can file an appeal if you have had a “life-changing event” in the last two years.

Life-changing events include:

- Marriage

- Divorce

- Retirement (you or your spouse)

- Reducing working hours (you or your spouse)

- Natural disaster, disease, fraud, or other involuntary loss of income-producing property

- Pension loss

- Employer’s bankruptcy

You can contact Social Security at +1 800-772-1213 and tell them you want to appeal your IRMAA bracket. Or, you can contact your local Social Security Office to find out what’s needed for the appeal.

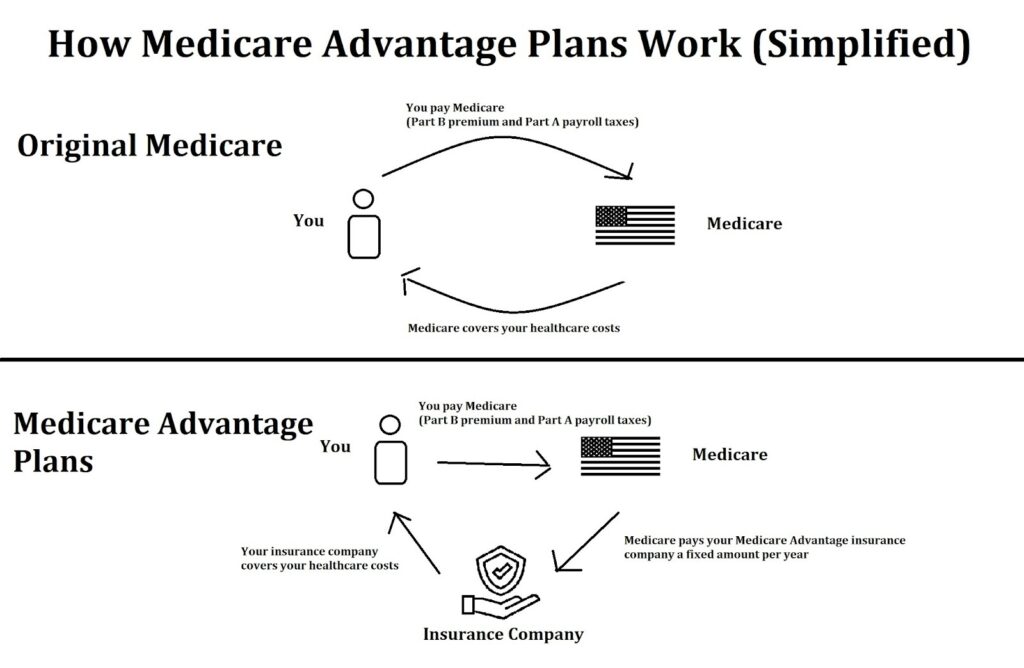

Mistake #10: Only Enrolling in Original Medicare

Medicare Part A (inpatient coverage) and Medicare Part B (outpatient coverage) are the foundation of Medicare. Together, these two parts are called Original Medicare.

Original Medicare typically covers roughly 80% of your total healthcare costs.

That’s great, but many people think that this is enough, so they don’t bother enrolling in anything else.

Big mistake.

You see, even though Original Medicare usually covers around 80% of your costs, there’s no cap on how much those costs are.

If you get a life-changing disease or condition, it’s not rare for your healthcare bill to reach over $100,000. If you’re responsible for 20% of that, you would have to pay at least $20,000!

To make matters worse, Original Medicare doesn’t cover most prescription medications either.

That’s why it’s so important to get additional coverage.

How to Avoid This Mistake

You could avoid this mistake by enrolling in either:

- Medicare Advantage Plan with a Prescription Drug Plan (MAPD)

- or a Medicare Supplement (Medigap) plan plus a Medicare Part D drug plan.

Here’s a quick comparison chart:

| Medicare Advantage Plans | Medicare Supplement Plans | |

| Premiums: | Typically Lower $0 – $200 ($18 average) | Typically Higher Medigap Plan G: $100 – $300Medigap Plan N: $80 – $250 |

| Network: | Most plans have networks of doctors and hospitals | Plans will cover you for any doctor or hospital that accepts Medicare |

| Coverage: | Typically no standardization As long as they cover everything in Medicare Part A and B, Advantage Plan coverage can vary | 10 standardized plans (Medigap Plan A, B, C, D, F, G, K, L, M, and N) All plans must provide the same coverage regardless of insurance company |

| Referrals and Prior Authorizations: | Usually yes | Usually no |

| Vision, Dental, and Hearing Benefits: | Usually yes | Usually no |

| Drug Coverage: | Usually included | Not included. You need to sign up for a separate Medicare Part D drug plan. |

| Costs: | More out-of-pocket costs Exact costs depend on your plan. Most include: DeductiblesCopaysCoinsurancesMaximum out-of-pocket limits | Less out-of-pocket costs Exact costs depend on which plan you choose. For example: Medigap Plan G: Medicare Part B Deductible only Medigap Plan N: Medicare Part B Deductible, copays for office and ER visits, Medicare Part B excess charges |

| Enrollment: | Can enroll during the ICEP, OEP, or SEP No medical underwriting process | Can enroll at any time. However, if you enroll outside your Initial Enrollment Period (six months after Medicare Part B starts), you may be subject to a medical underwriting process |

What’s better for you will depend on factors like your income, your health, and your location.

However, both of these help pay for the remaining 20% that Medicare doesn’t cover. And both help protect you from paying large bills out-of-pocket!

Mistake #9: Falling for Shiny Advertising Tactics

You’ve probably seen a few ads for “Medicare plans.”

Maybe they tell you that if you sign up today, you can get a FREE $3,000 Flex Card for groceries.

Or perhaps someone even called you on the phone and told you that if you sign up for this “brand-new Medicare plan,” you’ll get a ton of fantastic benefits that you’re missing out on.

If you find yourself in these situations, be wary!

While they’re not 100% scams (salespeople selling Medicare Advantage plans usually run these ads), enrolling in a plan for its extra benefits shouldn’t be your most important consideration.

This is because typically, these extra benefits are not truly free.

If you choose to enroll in a Medicare Advantage Plan, Medicare will send your insurance company a bulk amount of money for your healthcare coverage. It’s normally up to the insurance company to decide how to use this money to cover your healthcare costs.

If a plan uses the money for extra benefits like groceries, it won’t have as much available to use for your healthcare coverage.

That’s why, most of the time, the plans that offer the most extra benefits usually have the worst coverage.

How to Avoid This Mistake

Don’t get carried away!

Good salespeople can sway you to purchase plans that are against your best interests. They typically speak to your feelings and make lavish promises that are hard to resist.

That’s why whenever you see or receive an advertisement for a Medicare plan, always be skeptical.

Use your brain, not your heart. Look at the actual facts and numbers of the plan and compare them directly to your current plan.

You might find that your current plan is a better fit for you than what’s being offered.

Another good rule of thumb is to be wary of plans that come to you. You want to be the one to find a plan and approach them instead!

Mistake #8: Going Out of Network

This is a big one.

A lot of people sign up for Medicare Advantage Plans for their low premiums and great terms.

However, many people don’t realize that Medicare Advantage Plans have networks.

So they head to any random doctor for treatment, only to realize when the bill arrives that their plan doesn’t cover them!

If it happens to you, you’ll typically have to pay for your hospital bill 100% out-of-pocket.

How to Avoid This Mistake

When you’re choosing your plan, be sure your preferred doctors are in your network if you want to avoid extra costs.

And if you’ve already chosen a Medicare Advantage plan, check to see which doctors are in-network before visiting a doctor.

If you sign up for a Medicare Advantage Plan that doesn’t include convenient hospitals or doctors, even if all the other terms seem like a good fit for you…you might find you dislike your plan later.

Another way to avoid this mistake is to ask the hospital or doctor ahead of time if they accept your Medicare Advantage Plan.

Our team of licensed insurance agents can also check on these things for you.

Most Medicare Advantage Plans will cover your out-of-network costs if it’s a medical emergency.

But if it’s not an emergency, you should have enough time to find a hospital that accepts your MA plan.

Mistake #7: Not Shopping Every Year

Not grocery shopping, of course, but rather Medicare Plan shopping!

Every year, Medicare Advantage plans can change some of their terms.

Even if you decide to go the Medigap route, your Medicare Part D drug plan can also have yearly changes.

The mistake is just accepting these changes without reviewing them.

Sometimes, Medicare Advantage Plans and Medicare Part D drug plans can have drastic changes. And because many people don’t bother to read the changes, they renew their plan without realizing it’s different now.

They only realize things have changed when their out-of-pocket expenses arrive in the mail. Some people never even know they’re spending more at all!

How to Avoid This Mistake

Every year, right before the Annual Enrollment Period (Oct 15 – Dec 7), your Medicare Advantage Plan or Medicare Part D drug plan will send you a summary of changes for the following year.

Review this document!

If you find changes that you don’t like, you can shop around for another Medicare Advantage plan or Medicare Part D plan that better fits your needs.

You’re allowed to switch plans during the Annual Enrollment Period. And if you currently have a Medicare Advantage plan, you can also switch during the “Medicare Advantage Open Enrollment Period,” which runs from January 1 to March 31 every year.

Even if you are okay with the changes to your current plan, shopping around is generally a good idea.

Who knows, there might be a new plan on the market that fits your needs better.

Mistake #6: Relying 100% on Influencers

There’s a lot of great Medicare content on social media and YouTube.

But there’s one trend that a lot of YouTubers jump on:

Hating on Medicare Advantage Plans.

If you only listen to these influencers, you’ll believe that all MA plans are evil.

When you turn 65, you’ll blindly enroll in a Medicare Supplement plan without considering the alternative.

The truth is, there are many situations where choosing a Medicare Advantage plan could be the right fit for you.

They also tend to choose one MA horror story and paint it as if all MA plans are as bad as the one in their story.

In reality, as long as you choose a reputable insurance company, you will typically get the coverage you need.

How to Avoid This Mistake

We’re not saying Medicare Advantage Plans are better than Medigap Plans.

What we’re saying is that if someone’s biased, they might make more money if you sign up for the plan they’re selling.

Medicare Advantage plans and Medigap Plans both have their pros and cons.

The best way to avoid this mistake is to compare multiple plans.

Compare the plans available in your area. See what works for your unique situation.

Mistake #5: Staying in a “Downward Spiral” Plan When You Can’t Afford It

If you choose to go for a Medicare Supplement Plan, this is one mistake many people make.

A lot of people like the fact that Medigap plans have the same coverage regardless of which insurance company you enroll with, and they also don’t change terms every year (unlike Medicare Advantage plans).

However, this also forces Medicare to discontinue plans that no longer align with its goals. (Being discontinued means new people typically cannot enroll in the plan.)

Examples of this include Medigap Plan F and Medigap Plan C, which were discontinued in 2020. Looking further back, Medigap Plan J was also discontinued in 2010 (although people who already had Medicare before these plans “closed” can still enroll in one of these plans).

Now, here’s the problem:

When Medicare discontinues a Medigap Plan, it allows everyone on that plan to stay on it, and many people who like the plan choose to do so.

However, the plan goes into a “downward spiral” when there are no new enrollees.

Here’s what that means:

Insurance companies rely on healthy payors to put money into the plan, which they use to offset the healthcare costs for sick people on the plan.

With no new healthy enrollees, the pool of healthy payors naturally shrinks as people get older.

This typically forces the plan to raise premiums to help pay for everyone’s healthcare.

Therefore, the remaining people on Medigap Plan J typically see rising premiums, and people still on Medigap Plan C and F can expect the same in the years to come.

How to Avoid This Mistake

If you’re on a Medigap Plan, and Medicare discontinues it for whatever reason — then if you’re sensitive to price increases you might consider switching plans.

If the plan discontinues and you’re still healthy, switching plans shouldn’t be difficult.

If you already have a condition, you may have a harder time switching. A licensed insurance broker should help you with your available options.

Mistake #4: Assuming Your Drugs Are Covered

This might sound simple, but a lot of people make this mistake.

It’s not only the people who assume Original Medicare covers drugs (which is already too many people).

It’s also people who enroll in Medicare Advantage Plans or Medicare Part D drug plans who assume their drugs are covered without checking.

Remember, your Medicare Part D plan doesn’t cover all drugs.

Aside from a few regulations, each plan is free to decide which drugs it covers and which ones it doesn’t.

If your prescription medications aren’t part of your drug plan’s “formulary,” your plan typically won’t cover it.

Many people don’t realize this until it’s too late.

How to Avoid This Mistake

Each Medicare Part D drug plan publishes its formulary. This is the complete list of all the drugs it covers.

Before enrolling in a plan, make sure to check if your prescription medications are included!

It might sound simple, but too many people don’t do this.

Also, when you receive your annual summary of changes, make sure to check if your drugs are still included in your plan’s formulary!

Note: you can read more about how Medicare Part D drug plans work here!

Mistake #3: Missing the Medigap OEP

If you’re planning to enroll in a Medigap (Medicare Supplement) Plan, there’s one important period you should know about.

The Medigap Open Enrollment Period:

It runs for six months, starting on the day you’re enrolled in Medicare Part B.

During this period, you can enroll in any Medigap plan without a medical underwriting process.

By law, insurance companies selling Medigap plans cannot ask you health-related questions during this period. They also cannot charge you higher premiums due to a pre-existing condition.

This period only happens once.

If you miss it, you may not have another chance to enroll in Medigap without an underwriting process (in most states). There are some situations when you can also get a Medigap plan without underwriting using Guaranteed Issue Rights. However, Guaranteed Issue Rights are only for very limited circumstances.

How to Avoid This Mistake

The best way to avoid this is to know which plan you’ll enroll in before you turn 65.

Before you turn 65, you should already know the differences between Medicare Advantage plans and Medigap plans.

Too many people delay studying Medicare until after they’re 65.

By the time they realize they want a Medigap plan, it can be too late, and they may have to undergo the medical underwriting process.

Mistake #2: Doing Things On Your Own

Medicare is complicated.

People who try to do things on their own usually end up making costly mistakes.

And we can’t blame them.

The government didn’t do us any favors by how complex they made Medicare!

But you can get professional help for FREE.

We’re not just talking about free online resources that you can study on your own. If you need help finding the best plan for your needs, you can easily get help from a licensed insurance agent.

Unlike salespeople, licensed insurance agents have contacts with many insurance companies in your area. And their services are at no cost to you.

This way, they won’t be biased towards one plan. Instead, they can help you find the plan that best fits your needs.

Licensed insurance agents get their money through commissions, so you won’t have to pay a single cent to get their help!

How to Avoid This Mistake

You can chat with our licensed insurance agents by calling +1 877-360-6565 (TTY: 711) or booking an appointment here.

Of course, it’s always good to do some of your own research.

But when it’s time to look for plans in your area, give them a call so they can help you find and compare these plans and find the plan that best fits your needs.

Mistake #1: Missing The Most Important Enrollment Period

By far, the biggest mistake people make when it comes to Medicare is not enrolling on time.

If you already know about Medicare’s late enrollment penalties, this might seem a bit anticlimactic to you.

But when you see how many people are late enrolling in Medicare, you’ll understand why this is the #1 mistake.

If you didn’t know, Medicare typically imposes PERMANENT penalties on your premiums if you enroll late.

That is an extra 10% on your Medicare Part B premium for every year you miss and an additional 1% on your Medicare Part D premium for every month you miss.

These penalties are permanent, so typically they will never go away for as long as you have Medicare (which is essentially the rest of your life).

That’s why it’s so important to be aware of your enrollment periods!

Your Initial Enrollment Period (IEP) starts three months before your 65th birth month and ends three months after your 65th birth month. You can enroll in Medicare Parts A and B during this time, as well as Medicare Part D.

If you miss this, you’ll get the Medicare Part B and D penalties (except for a few exceptions, like if you’re covered by your employer’s health plan).

How to Avoid This Mistake

Once again, the best way to avoid this mistake is to study Medicare ahead of time.

By reading this article, you’re already doing yourself a big favor.

Getting hit by the permanent late enrollment penalties is painful. And it’ll never go away!

Also, remember that in order to avoid penalties, you’ll typically want to enroll in a Medicare Part D plan when you first become eligible, even if you aren’t taking prescription medications yet.

Conclusion

There are a lot of mistakes you can make when it comes to Medicare.

But at the end of the day, the real solution is education.

When you understand exactly how Medicare works, you can avoid not only these 15 Medicare mistakes but also any potential mistakes that can pop up in the future.

That’s why if you want to learn all about Medicare, view our Medicare workshop.

In it, we go over everything you need to know to get started in Medicare.

We’ll explain how to find and choose plans and discuss other potential pitfalls that you should avoid.

So, if you want to make the most of Medicare, view our workshop below!

Calvin Bagley is the founder of PlanFit, The Medicare Store, and Nuvo Health. He and his team have helped over 60,000 people navigate Medicare options, and he’s a nationally recognized speaker in the Medicare industry. Most importantly, he’s someone who believes every American deserves clear, honest information without pressure.