- Original Medicare only covers around 80% of your healthcare costs, which is why most people are encouraged to enroll in either a Medicare Advantage Plan or a Medicare Supplement (Medigap) Plan.

- Both Medicare Advantage Plans and Medicare Supplement (Medigap) Plans are provided by private insurance companies working with Medicare. They both help reduce your out-of-pocket healthcare costs.

- Medicare Advantage Plans typically have lower premiums, and usually also include prescription drug coverage and other perks (like coverage for dental, vision, and hearing care).

- Medicare Supplement (Medigap) Plans typically have higher premiums, and you may need to enroll in a separate Part D prescription drug plan for drug coverage. However, Medicare Supplement (Medigap) Plans usually allow you to see any doctor or hospital that accepts Medicare.

- What’s best depends on your specific needs, your location, and the plan options in your area. Read below to learn more about how to choose the better plan fit for you!

One of the biggest Medicare decisions you may have to make is choosing between a Medicare Advantage Plan and a Medicare Supplement (Medigap) Plan.

If you look online, you’ll find this topic very hotly debated. People have all kinds of opinions on both sides, and there’s plenty of overpromising and fearmongering, especially from sales agents selling one type over the other.

But here’s the truth:

When it comes to Medicare Advantage Plans vs Medicare Supplement (Medigap) Plans, the “best” option all depends on what’s right for YOU.

It depends on your specific needs, situation, and even location.

That’s why in this article, we’ll cut through the opinions, and give you all the facts you need to know about Medicare Advantage Plans and Medicare Supplement (Medigap) Plans.

We’ll compare coverage, costs, and your provider options for both, so by the end of this article, you’ll have a much better idea of which plan could be the best fit for you!

Quick Refresher: Why You Need Additional Coverage

Before we start comparing Medicare Advantage Plans and Medicare Supplement (Medigap) Plans, let’s take a quick refresher on why it’s a good idea for most people to enroll in one of the plans in the first place.

Original Medicare (Parts A and B) usually only covers roughly 80% of your healthcare expenses. This means that you’re responsible for paying the remaining 20% out-of-pocket (and there’s no limit on how expensive this 20% can get).

Medicare Advantage Plans and Medicare Supplement (Medigap) plans both help reduce your out-of-pocket spending for Medicare. These plans are provided by private insurance companies, and you need to be enrolled in Original Medicare before signing up for either option.

However, that’s about where the similarities end. Let’s take a closer look at what makes these two types of plans so different!

Medicare Advantage Plans vs Medicare Supplement (Medigap) Plans

| Medicare Advantage Plans | Medicare Supplement Plans | |

| Covers | Everything in Original Medicare (Part A and B) Prescription drug coverage (most plans) Dental, vision, and hearing care (some plans) Other perks | Most of the out-of-pocket expenses in Original Medicare (Part A and B) |

| Plan Options | HMO PPO PFFS SNP MSA | 10 standardized plans: Medigap Plan A, B, C, D, F, G, K, L, M, and N |

| Cost | $0 – $200+/month (Average $18.5/month according to the KFF) Deductibles and copays (varies by plan) Maximum out-of-pocket (varies by plan) | Depends on plan type, location, age, and other factors Plan G: roughly $100 – $300/month* Plan N: roughly $70 – 270/month* |

| Doctors and Hospitals | Typically has networks of local doctors and hospitals May require referrals or prior authorizations for special treatment | Any doctor or hospital that accepts Medicare Typically doesn’t require referrals or prior authorizations |

| Annual Changes | Plans typically change terms every year | Coverage usually doesn’t change, but prices may increase every year |

| Enrollment Periods | Initial Enrollment Period (IEP) Annual Election Period (AEP) Medicare Advantage Open Enrollment Period (MA OEP) Special Enrollment Periods (SEPs) No medical underwriting | Medigap Open Enrollment Period (OEP) Special Enrollment Periods (SEPs) May require medical underwriting if you enroll outside your Medigap OEP or a SEP |

*These are rough estimates. Price range varies by age, location, and other factors. To find accurate price ranges, chat with a licensed insurance agent at no cost to you.

The main difference between these types of plans is that when you enroll in a Medicare Advantage Plan, Medicare will normally transfer the responsibility of your healthcare to your insurance provider. They pay them a fixed amount per year, and your Medicare Advantage Plan chooses how they use that money for your healthcare.

This is why some Medicare Advantage Plans can offer $0 premiums. It’s also why they can typically provide more coverage and extras than Original Medicare.

On the other side, if you enroll in a Medicare Supplement (Medigap) Plan, Medicare is still responsible for your healthcare. Your Medicare Supplement (Medigap) Plan insurance company will typically only help cover your out-of-pocket costs with Original Medicare, but not provide extra coverage (such as prescription drugs).

Medicare Supplement (Medigap) Plans usually cost more since they don’t receive payment from Medicare. Depending on which Medigap plan you choose, your out-of-pocket costs are typically lower.

Still not sure what’s right for you?

Let’s take a closer look at the differences!

Coverage

Medicare Advantage Plans are private insurance that must cover everything Original Medicare covers. Aside from that, MA plans may add as much additional coverage as they want.

Medicare Supplement Plans are private insurance but are standardized by Medicare. They help pay for your out-of-pocket expenses in Original Medicare.

| Medicare Advantage | Medicare Supplement | |

| Covers | Everything in Original Medicare (Part A and B) Prescription drug coverage (most plans) Dental, vision, and hearing care (some plans) Other perks | Some of the out-of-pocket expenses in Original Medicare (Part A and B) |

Medicare Advantage Plans are required to include everything in Original Medicare. Apart from this, insurance companies offering Medicare Advantage Plans have the flexibility to decide what else they cover.

Most Medicare Advantage Plans include a built-in Part D prescription drug plan—they may also include coverage for dental, vision, and hearing care (three things that Original Medicare typically doesn’t cover).

Many Medicare Advantage Plans also include extra perks like gym memberships, no-cost transportation to the hospital, Flex Cards for groceries, and more.

Medicare Supplement (Medigap) Plans help cover the out-of-pocket expenses of Original Medicare. Remember, Original Medicare usually only covers roughly 80% of your healthcare costs.

There are six “gaps” in Original Medicare that you’re responsible for paying out-of-pocket. These are:

- Medicare Part A deductible

- Hospital stay copays

- Skilled nursing facility stay copays

- Medicare Part B deductible

- Medicare Part B coinsurance

- Medicare Part B excess charges

When you sign up for a Medicare Supplement (Medigap) Plan, your insurance company should help pay for some of these six gaps, depending on the type of plan you get.

For example: Medigap Plan G pays for 5 out of these 6 gaps. Your only out-of-pocket responsibility with Original Medicare and Plan G is usually the Part B deductible (which costs $240 in 2024).

However, Medicare Supplement (Medigap) Plans typically don’t have additional coverage. You may have to enroll in a Part D prescription drug plan separately to get drug coverage.

Plan Options

There are five types of Medicare Advantage Plans. These are not standardized, meaning they can offer as much as they want to.

Meanwhile, Medicare Supplement (Medigap) Plans come in ten standardized plans—so you should get the same level of coverage regardless of your insurance company.

| Medicare Advantage | Medicare Supplement | |

| Plan Options | HMO PPO PFFS SNP MSA | 10 standardized plans: Medigap Plan A, B, C, D, F, G, K, L, M, and N |

The main types of Medicare Advantage Plans include:

- Health Maintenance Organization (HMO): This is one of the most common types of MA plans. HMOs typically provide low-cost healthcare as long as you stay within your plan’s network.

- Preferred Provider Organization (PPO) – This is another common type of MA plan. PPO plans typically cover you for out-of-network services(although you may have higher copays if you do so).

- Private Fee-for-Service (PFFS) – PFFS plans typically have no network, but require your healthcare provider to agree to your plan’s terms before you can get treatment.

- Special Needs Plan (SNP) – SNPs can be either HMOs or PPOs. These plans are usually designed for people with qualifying health disorders or people with Medicaid.

- Medicare Savings Account (MSA) – MSAs work similarly to Health Savings Accounts (HSAs). They typically don’t have a network or cover prescription drugs.

The ten standardized Medicare Supplement Plans include Plans A, B, C, D, F, K, L, M, and N. Here’s a quick chart from Medicare.gov showing what each plan covers:

Since these plans are standardized, it doesn’t matter which insurance company you get your Plan G (or any other plan type) from, they should provide the same level of coverage.

According to the AHIP, Medigap Plans F, G, and N are the three plans that most people opt for.

Costs

Medicare Advantage Plans can cost anything from $0 – $200+ a month, with the average being roughly $18.5/month according to the KFF. MA plans typically have their own set of deductibles, copays, and maximum out-of-pocket costs.

Meanwhile, the monthly cost of Medicare Supplement (Medigap) Plans depends on the plan type, your location, and other factors.

| Medicare Advantage | Medicare Supplement | |

| Cost | $0 – $200+/month (Average $18.5/month according to the KFF) Deductibles and copays (varies by plan) Maximum out-of-pocket (varies by plan) | Depends on plan type, location, age, and other factors Plan G: roughly $100 – $300* Plan N: roughly $70 – 270* |

*These are rough estimates. Price range varies by age, location, and other factors. To find accurate price ranges, chat with a licensed insurance agent at no cost to you.

Because Medicare pays Medicare Advantage Plans to cover you, many MA plans have low or even $0 premiums. According to the KFF, the average cost for Medicare Advantage Plans in 2024 is around $18.5/month.

When you enroll in a Medicare Advantage Plan, you usually no longer have to worry about the deductibles, copays, and coinsurance of Original Medicare. However, your plan should have its own set of cost-sharing methods.

Most MA plans have:

- Deductibles – The amount you have to spend out-of-pocket before your plan starts covering you.

- Copays – A cost-sharing method where you pay a fixed amount (ex: $20) for an item or service, while your plan covers the remaining balance.

- Coinsurance – A cost-sharing method where you pay a percentage (ex: 20%) of the costs for items or services, while your plan covers the remaining balance.

- Maximum Out-of-Pocket Limits (MOOP) – Once your out-of-pocket spending reaches your plan’s MOOP amount, your plan will typically cover your in-network healthcare costs for the rest of the year

To give you an idea of the costs of a Medicare Advantage Plan, here are some sample plans from Indianapolis, Indiana (which has pretty average prices compared to the rest of the country).

Note: In some cities, prices are higher than this sample. While in other parts of the country, they’re cheaper.

| Medicare Advantage Plan Sample Costs in Indianapolis, Indiana* | |||

|---|---|---|---|

| Sample Plan #1 (HMO) | Sample Plan #2 (PPO) | Sample Plan #3 (Regional PPO) | |

| Premium: | $0 | $27 | $73 |

| Deductible: | Health: $0 Drugs: $0 | Health: $0 Drugs: $0 | Health: $500 Drugs: $0 |

| MOOP: | $3,100 | $3,800 (in-network) $5,750 (in and out-of-network) | $6,400 (in-network) $10,000 (in and out-of-network) |

| Inpatient copays or coinsurance: | $340/day (day 1-6)$0 (day 7-90) | In-network:$370/day (day 1-5)$0 (day 6 onwards) Out-of-network:40% per stay | In-network:$290/day (day 1-7)$0 (day 8-90) Out-of-network:30% per stay |

| Outpatient copays or coinsurance: | $350 per visit | In-network:$0 – $370 copay per visit Out-of-network:$400 copay per visit | In-network:$0 copay or 20% coinsurance per visit Out-of-network:40% coinsurance per visit |

| Other Coverage: | ✅ Drugs✅ Vision✅ Dental✅Hearing | ✅ Drugs✅ Vision✅ Dental✅Hearing | ✅ Drugs✅ Vision✅ Dental❌Hearing |

*The plans and numbers shown were taken from Medicare’s plan finder tool for sample purposes. Also, the details below are just some of the numbers of these plans.

The costs of Medicare Supplement (Medigap) Plans work differently from Medicare Advantage Plans.

Remember, with a Medicare Supplement (Medigap) Plan, you’ll still be on Original Medicare. You just have a plan to help you pay for the gaps!

Here’s a quick rundown of the typical out-of-pocket costs of Original Medicare:

| Medicare Costs in 2024 (Taken from Medicare.gov) | |

| Part A | Premium: $0 for most people Deductible: $1,632 Inpatient hospital copays:Day 1 – 60: $0Day 61 – 90: $408/dayDay 91 – 150: $816/day (using lifetime reserve days)Day 151 onwards: You pay 100% Skilled nursing facility copays:Day 1 – 20: $0Day 21 – 100: $204/dayDay 100 onwards: You pay 100% |

| Part B | Premium: $174.7 (base premium) Deductible: $240 Most items and services: 20% coinsurance |

*Items covered by Part B may also sometimes have excess charges

When you get a Medicare Supplement Plan, you’ll pay an insurance company every month to cover these out-of-pocket expenses of Medicare.

How much your plan costs depends on the insurance company, your location, your age, whether you’re male or female, whether you use tobacco, and whether you have a household discount (some other factors may apply).

Here are some monthly costs from different cities around the country:

| Medigap Plan G | Medigap Plan N | Medigap Plan K | |

| San Francisco, California | $132 – $211 | $101 – $171 | $53 – $123 |

| New York City, New York | $302 – $776 | $220 – $483 | $99 – $225 |

| Indianapolis, Indiana | $111 – $448 | $85 – $436 | $63 – $157 |

| Boise, Idaho | $164 – $280 | $117 – $230 | $67 – $182 |

| Houston, Texas | $132 – $571 | $103 – $519 | $71 – $177 |

*costs taken from Medicare’s plan finder tool for a 65-year-old male who doesn’t smoke tobacco and doesn’t have household discounts on April 2024

If you want a closer look at what these plans cover and how much they cost, read this article on Plan G vs Plan N article (since those are the two popular plans today). But here’s a quick overview of what both plans cover:

| Benefit | Plan G | Plan N |

| Part A coinsurance and hospital costs up to an additional 365 days after Medicare’s benefits are used | ✔️ | ✔️ |

| Part B coinsurance and copayment | ✔️ | ✔️ (with copays) |

| Blood (first 3 pints) | ✔️ | ✔️ |

| Part A hospice care coinsurance or copayment | ✔️ | ✔️ |

| Skilled nursing facility care coinsurance | ✔️ | ✔️ |

| Part A deductible | ✔️ | ✔️ |

| Part B deductible | ❌ | ❌ |

| Part B excess charge | ✔️ | ❌ |

| Foreign travel emergency (up to plan limits) | 80% | 80% |

| Out-of-pocket limit | N/A | N/A |

This means with a Plan G, your out-of-pocket spending will typically only be the Part B deductible, (which is set to $240 for 2024). Meanwhile, with a Plan N, you’ll have to make copays for doctor’s office and ER visits (and you may have to pay Part B excess charges)

Doctors and Hospitals

Medicare Advantage Plans usually have a network of doctors and hospitals where you can get low-cost healthcare. You may have to pay higher copays if you get services outside your plan’s network (except in emergencies). Additionally, referrals or prior authorizations may be required for specialized treatments.

Medicare Supplement (Medigap) Plans should help you cover your expenses for any doctor or hospital that accepts Medicare. These plans typically don’t require referrals or prior authorizations for your insurance company to cover your costs.

| Medicare Advantage | Medicare Supplement | |

| Doctors and Hospitals | Typically has networks of local doctors and hospitals May require referrals or prior authorizations for special treatment | Any doctor or hospital that accepts Medicare Typically doesn’t require referrals or prior authorizations |

Medicare Advantage Plans usually partner with local doctors and hospitals to offer low-cost healthcare. This is their “network.”

If you enroll in an HMO, you may not be covered if you go outside your plan’s network except in emergencies. In contrast, PPO plans usually cover you for out-of-network doctors and hospitals, but your copays may be higher.

Some Medicare Advantage Plans also have coverage for traveling (both local and international travel). However, if you are planning to move to another part of the country, you may want to switch to another Medicare Advantage Plan based in your new area.

Medicare Advantage Plans could also require referrals to see a specialist, or prior authorizations if you need special treatment.

Medicare Supplement (Medigap) Plans don’t have networks. Any doctor or hospital that accepts Medicare should accept your Medicare Supplement (Medigap) Plan, and cover you across the country. Some Medigap plans also have coverage for foreign travel emergencies.

You also typically won’t need referrals or prior authorizations from your insurance company with Medicare Supplement Plans. If your doctor deems a procedure medically necessary, Medicare and your Medicare Supplement Plan will normally cover the costs.

Annual Changes

Medicare Advantage Plans usually change their terms every year. This may include their cost, cost-sharing, network of doctors and hospitals, and the prescription drugs they cover.

Medicare Supplement (Medigap) Plans typically don’t change their coverage but may increase the pricing of their plan every year.

| Medicare Advantage | Medicare Supplement | |

| Annual Changes | Plans typically change terms every year | Coverage doesn’t change, but prices may increase every year |

Enrollment

You can enroll in a Medicare Advantage Plan when you first become eligible for Medicare. Medicare Advantage Plans also have a few enrollment periods every year when you can join or switch plans. You can typically join Medicare Advantage Plans even with pre-existing health conditions (no medical underwriting).

You may also enroll in a Medicare Supplement (Medigap) Plan when you first become eligible for Medicare. These plans have a Medigap Open Enrollment Period where you can enroll in any plan without medical underwriting. If you miss your Medigap OEP and don’t qualify for a Special Enrollment Period, you may have to undergo medical underwriting.

| Medicare Advantage | Medicare Supplement | |

| Enrollment Periods | Initial Enrollment Period (IEP) Annual Election Period (AEP) Medicare Advantage Open Enrollment Period (MA OEP) Special Enrollment Periods (SEPs) No medical underwriting | Medigap Open Enrollment Period (OEP) Special Enrollment Periods (SEPs) May require medical underwriting if you enroll outside your Medigap OEP or a SEP |

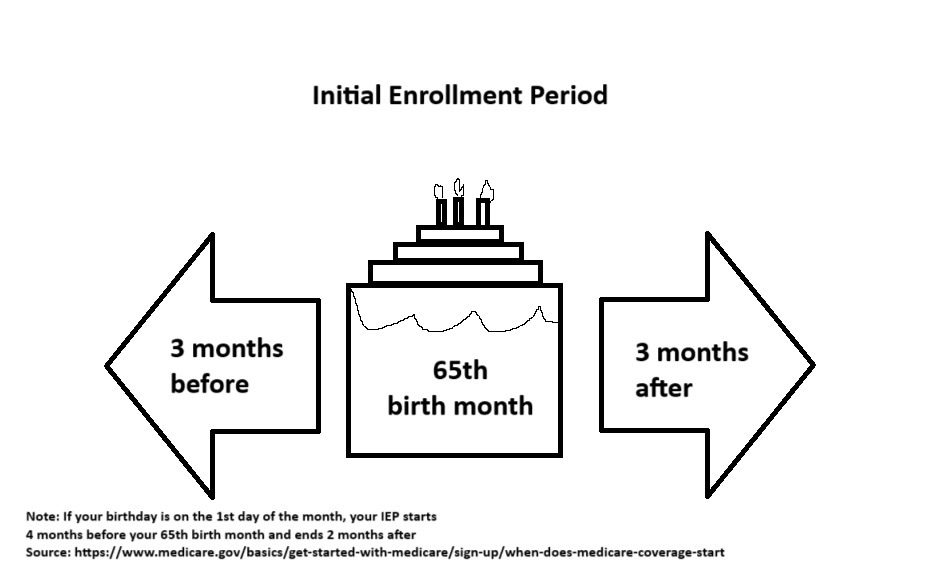

The Initial Enrollment Period (IEP) for Medicare Advantage Plans is the same IEP as Medicare. It’s a 7-month period that starts 3 months before the month you turn 65, and ends 3 months after the month you turn 65.

If you miss this period, you may also join a Medicare Advantage Plan during the Annual Election Period (AEP). According to Medicare.gov, this period runs from October 15 to December 7 every year. If you’re switching from a Medicare Supplement (Medigap) Plan to Medicare Advantage, this is usually the time you can do this.

If you already have a Medicare Advantage Plan and would like to switch to a different plan, you can also do so during the Medicare Advantage Open Enrollment Period. This typically runs from January 1 to March 31 every year.

Finally, there are several Special Enrollment Periods (SEPs) when you can enroll in or switch to another Medicare Advantage Plan. One example of an SEP would be if you transfer to another state. You can find a full list of SEPs on Medicare.gov.

You typically won’t have to worry about medical underwriting with Medicare Advantage Plans. This means that you can enroll in a plan even if you have pre-existing health conditions.

With Medicare Supplement (Medigap) Plans, you can also enroll during your IEP. However, there’s an important enrollment period you need to be aware of with Medigap Plans. This is the Medigap Open Enrollment Period, which runs for 6 months once your Part B coverage starts.

During this period, you can enroll in any Medicare Supplement (Medigap) Plan, and Medigap insurance companies are not allowed by law to have a medical underwriting process or charge you more than the preferred rate. This means you can enroll in a Medigap plan even with pre-existing health conditions.

If you miss the Medigap Open Enrollment Period, you can enroll in a Medicare Supplement (Medigap) Plan at any time. However, in most states, Medigap insurance companies may put you through a medical underwriting process if you enroll outside the Medigap OEP. They may also be able to charge you more for the plan if you have a pre-existing condition.

Because of this, it may be difficult to switch from a Medicare Advantage Plan to a Medicare Supplement (Medigap) Plan if you already have a health condition.

What’s Better? Medicare Advantage or Medicare Supplement Plans?

Now for the BIG question:

What’s better?

This might be an anti-climactic answer, but the truth is it really depends on YOU.

By reading this article, we hope you have a much better idea of how these two types of plans work, and how they differ from one another.

If you need more help deciding, don’t hesitate to reach out to our team of licensed insurance agents! You can call or text us at +1 877-360-6565 (TTY: 711) and get assistance at no cost to you.

Our team here at PlanFit would be more than happy to assist in finding the right plan fit for YOU!

Calvin Bagley is the founder of PlanFit, The Medicare Store, and Nuvo Health. He and his team have helped over 60,000 people navigate Medicare options, and he’s a nationally recognized speaker in the Medicare industry. Most importantly, he’s someone who believes every American deserves clear, honest information without pressure.