- Some Medicare-enrolled healthcare providers may charge up to 15% more than the Medicare-approved amount. This is known as the Medicare Part B excess charge.

- Without additional coverage, you are responsible for paying Medicare Part B excess charges 100% out-of-pocket.

- You can easily check which healthcare providers in your area accept the Medicare-approved amount using Medicare’s provider finder tool.

- Medicare Supplement plans F and G typically cover Medicare Part B excess charges, while Medicare Advantage Plans have different cost-sharing schemes that generally don’t have Medicare Part B excess charges.

If you’ve been studying your Medicare costs, one term you’ve probably come across is “Medicare Part B excess charges.”

Maybe you’ve seen this when comparing your Medicare Supplement Plan options, or perhaps someone warned you about only going to doctors who accept “Medicare Assignment” to avoid these charges.

Whatever the case, knowing about Medicare Part B excess charges can potentially save you a lot of money.

That’s why, in this article, we’ll go over what Medicare Part B excess charges are, how they’re calculated, and how common they are.

We’ll also discuss a few ways you can potentially avoid these altogether, which isn’t too difficult to do.

As the founder of NuvoHealth, The Medicare Store, and the CEO of PlanFit, my team and I have helped thousands of people save money on Medicare. We hope this article helps you do just that by avoiding the Medicare Part B excess charge!

What is Medicare Part B?

To understand Medicare Part B excess charges, let’s first have a quick refresher on what Medicare Part B is.

Medicare Part B is the branch of Medicare that covers your medical costs. Medicare Part B covers medically necessary services, preventive services, durable medical equipment, and several other items and services.

Once you’ve paid the Medicare Part B deductible, Medicare will typically pay 80% of the cost for Medicare Part B items and services. It should cover your expenses as long as your healthcare provider accepts Medicare.

What Are Medicare Part B Excess Charges?

Medicare Part B excess charges come up when healthcare providers that accept Medicare charge more than the Medicare-approved amount. Some providers can charge up to 15% more than the Medicare-approved amount for items and services covered by Medicare.

Without additional coverage (such as a Medicare Supplement plan), you’re typically required to pay Medicare excess charges 100% out-of-pocket.

Thankfully, most healthcare providers that accept Medicare also stick to the Medicare-approved amount, known as “Medicare Assignment.”

What is Medicare Assignment?

Medicare Assignment is an agreement between Medicare and healthcare providers to charge Medicare’s approved pricing. Providers that accept Medicare Assignment cannot charge extra for Medicare-covered items and services.

There are generally 3 types of healthcare providers:

- Participating Providers – These providers typically accept Medicare Assignment. They submit your claim directly to Medicare and can only charge you for the Medicare Part B deductible and coinsurance when applicable. Participating providers typically wait for Medicare to pay its share before billing you for your share of the costs.

- Non-Participating Providers – These providers are enrolled in Medicare but don’t accept Medicare Assignment. They may or may not charge more than the Medicare-approved amount (up to 15% more). Also, when you go to a non-participating provider, you may have to pay upfront and then request a reimbursement from Medicare.

- Opt-Out – Providers who opt out of Medicare may charge you as much or as little as they choose. Opting out of Medicare means these providers don’t accept Medicare. Medicare will usually not cover services you receive from an opted-out provider except in emergencies.

How Expensive Are Medicare Part B Excess Charges? (Example Numbers)

To demonstrate how Medicare Part B excess charges work, let’s make an example situation:

Let’s say you need a specific treatment, and the Medicare-approved amount for said treatment is $500. Let’s also say this is your first Medicare-covered service for the year, so you haven’t met your Medicare Part B deductible yet ($283 in 2026).

Finally, in this example, let’s say you don’t have any additional coverage (such as a Medicare Supplement Plan or Medicare Advantage Plan) besides Original Medicare.

Here’s how different types of providers may charge you:

| EXAMPLE ONLY: Medicare Part B excess charges with unpaid deductible | |||

| Cost of Treatment | Medicare Pays | Your Out-of-Pocket Cost | |

| Participating Provider | $500 (Medicare-approved amount) | $173.60 80% of $500 – $240 (Part B deductible) | $326.40 $283 (Part B deductible) + 20% of remaining balance |

| Non-Participating Provider | Up to $575 (up to 15% more than the Medicare-approved amount) | $173.60 80% of $500 – $240 (Part B deductible) | Up to $401.40 $283 (Part B deductible) + 20% of remaining Medicare-approved amount + full excess charge |

| Opt-Out | Any | $0 | 100% |

In this example, you’ll have to pay $326.40 out-of-pocket with a participating provider since you haven’t reached the Medicare Part B deductible yet. If you’ve already reached this, then your out-of-pocket spending will be significantly lower (typically only 20% of total costs—$100 in this example).

The non-participating provider in this example can charge up to $575 for the treatment (15% of $500), but keep in mind that they may charge lower. Since you’re responsible for paying the full excess amount, you may have to spend up to $401.40 with a non-participating provider in this example. Take note of how Medicare pays the same regardless of whether the provider is participating or non-participating. Also, keep in mind that excess charges don’t count towards your Medicare Part B deductible.

Providers that opt out of Medicare can charge you any amount for the same treatment, and you’re typically responsible for paying the bill 100%.

Now, let’s take a look at another example. This time, let’s say the Medicare-approved amount is $1,000, and let’s say you’ve already met your Medicare Part B deductible:

| EXAMPLE ONLY: Medicare Part B excess charges with paid deductible | |||

| Cost of Treatment | Medicare Pays | Your Out-of-Pocket Cost | |

| Participating Provider | $1,000 (Medicare-approved amount) | $800 (80% of $1,000) | $200 (20% of $1,000 since the Part B deductible is already met) |

| Non-Participating Provider | Up to $1,150 (up to 15% more than the Medicare-approved amount) | $800 (80% of $1,000) | Up to $350 (20% of $1,000 + full excess charge) |

| Opt-Out | Any | $0 | 100% |

Note: This section is an example only made to demonstrate how Medicare Part B excess charges work. Please contact your healthcare provider to learn how they charge for your treatment.

Should You Worry About Medicare Part B Excess Charges?

Only in a few circumstances. According to a study by the KFF, around 96% of Medicare-registered healthcare providers accept Medicare Assignment. This leaves a mere 4% of Medicare-registered providers that can charge you more than the Medicare-approved amount.

Normally, it’s relatively easy to avoid excess charges, especially if you know how to spot them (more on this below!).

In some states, healthcare providers are also not allowed to have excess charges. While in other states, the limit is lower than 15%.

Which States Don’t Allow Medicare Part B Excess Charges?

Connecticut, Massachusetts, Minnesota, New York, Ohio, Pennsylvania, Rhode Island, and Vermont limit or disallow Medicare Part B excess charges.

However, the limits vary by state. In some states like Connecticut, healthcare providers aren’t allowed to have excess charges for people who are enrolled in a QMB (Qualified Medicare Beneficiary) program only (everyone else may receive excess charges) — while in states like Massachusetts, all Medicare-registered providers can’t have excess charges.

If you live in one of these states, make sure to check your local regulations!

How to Avoid Medicare Part B Excess Charges

There are generally three ways to avoid Medicare Part B excess charges:

- Find out whether a provider accepts Medicare Assignment by asking them or by using Medicare’s tool,

- enroll in a Medicare Supplement plan that covers Medicare Part B excess charges, or

- enroll in a Medicare Advantage Plan.

Let’s take a closer look.

How to Know If a Healthcare Provider Accepts Medicare Assignment

The simplest way to learn whether a healthcare provider accepts Medicare Assignment is by asking!

You first should ask if the provider accepts Medicare. Remember, if a provider opts out, Medicare usually won’t cover any of their services except in emergencies.

Once you confirm they accept Medicare, you can ask them if they accept the Medicare-approved amount (or “Medicare Assignment” if you want to use insurance jargon).

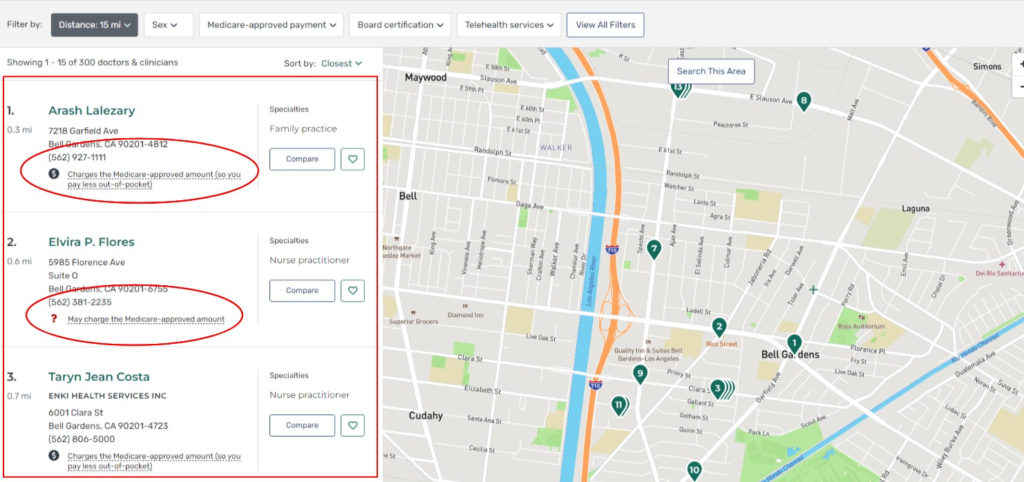

You can also use Medicare’s provider finder tool.

With it, all you have to do is enter your zip code, and it’ll give you a list of healthcare providers in your area.

Below are the contact details of each provider, and you’ll see whether they accept the Medicare-approved amount or not.

Medicare’s provider finder tool also allows you to search for providers in your area by name. So you can easily check if the doctor you’re seeing accepts the Medicare-approved amount (or Medicare Assignment).

Again, the KFF estimated that only 4% of Medicare-registered providers don’t accept Medicare Assignment, so more often than not, your doctor should accept the Medicare-approved amount.

However, it’s still a good idea to ask or check because the excess charges can get expensive.

Do Medicare Supplement Plans Cover Medicare Part B Excess Charges?

Some Medicare Supplement (Medigap) plans typically cover Medicare Part B excess charges. Of the ten available Medicare Supplement plans today, only Medigap Plan F and Medigap Plan G do.

If you’re enrolled in Medigap Plan F or Medigap Plan G, you can go to any healthcare provider that accepts Medicare, and your Medicare Supplement insurance should usually cover any excess charges. This is regardless of whether the healthcare provider accepts Medicare Assignment or not.

Note: Remember that Medigap Plan F is no longer available for people who turned 65 on or after January 1, 2020.

Do Medicare Advantage Plans Cover Medicare Part B Excess Charges?

When you enroll in a Medicare Advantage Plan, your insurance company sets its own deductibles and copays for when you get services. You will no longer be subject to Medicare Part B’s deductible, coinsurance, and excess charges.

Medicare Advantage Plans usually have a network of doctors and hospitals. You can typically get low-cost services when you stay within your Medicare Advantage Plan’s network.

If you go outside your plan’s network, you might have to pay higher copays (if you have a “PPO” plan), or you might not be covered by your plan unless it’s an emergency (if you have an HMO plan). So this can somewhat resemble an “excess charge” for Medicare Advantage Plans (although they’re not the same thing).

To learn more about how Medicare Advantage Plans work, read our full article about Medicare Advantage Plans here!

Conclusion: Ready to Take On Medicare?

Medicare Part B excess charges are rare, but they’re one of the many little things in Medicare that—if you’re unaware of—can cost you a lot of money.

That’s why learning about Medicare and all the potential pitfalls is critical, especially if you’re about to turn 65 soon!

That’s also why we put together a FREE comprehensive Medicare workshop.

In it, we go over everything you need to know to get started with Medicare, including an overview of Medicare Supplement vs. Medicare Advantage, when you should enroll to avoid penalties, and also a number of tips on how you can save money on Medicare.

You can sign up for the free workshop below:

Calvin Bagley is the founder of PlanFit, The Medicare Store, and Nuvo Health. He and his team have helped over 60,000 people navigate Medicare options, and he’s a nationally recognized speaker in the Medicare industry. Most importantly, he’s someone who believes every American deserves clear, honest information without pressure.