You’ve probably seen ads pushing you to call a number to sign up for the Medicare Giveback Program.

Maybe you’ve seen some that say that if you call now, you could get $144 or more off your Medicare premiums.

Is there a catch, or is it too good to be true?

Well…it’s complicated.

You see, Medicare Giveback Programs are a real thing.

However, insurance salespeople often use them as an advertising tool. They often exaggerate how much money you can get and rarely mention the downsides.

That’s why we’ll clarify givebacks for you in this article and show you how to tell whether or not choosing a Medicare Advantage Plan with one of these programs is worth it.

At the end, we’ll also show you other ways to save money on your Medicare Part B monthly payments.

Key Takeaways:

- The Medicare Giveback Program is a benefit offered by some Medicare Advantage Plans. It is provided by private insurance companies and is not a government assistance program.

- Most people have to pay $202.90/month for Medicare Part B in 2026. If you sign up for a Medicare Advantage Plan with a Medicare Giveback Program, you can get a reduced rate.

- Many Medicare Giveback Programs take $10-25 off your Medicare Part B premium, a few may remove around $144 or more, and some rare ones could cover the entire premium.

- Availability depends on the Medicare Advantage Plan insurance companies in your area. If a company offers this benefit, you can sign up for it. There is no qualifying process.

- Medicare Giveback Programs are also called Medicare Part B Giveback, Senior Giveback Plans, Social Security Giveback, and Medicare Part B Premium Reduction Benefits. These are all the same thing.

What Are Medicare Giveback Programs?

The Medicare Giveback Program is a feature included in some Medicare Advantage Plans. With it, you usually get $10-25 off your Medicare Part B premium, while some rare Medicare Advantage Plans may pay for the entire premium ($202.90 in 2026).

It’s important to note that despite its name, Medicare Giveback Programs are not government handouts. You join this program by enrolling in a Medicare Advantage Plan provided by a private insurance company.

How Do Medicare Giveback Programs Work?

To fully understand how the Medicare Giveback benefit works, you first need to understand the Medicare Part B monthly payment and Medicare Advantage Plans.

What is the Medicare Part B Premium?

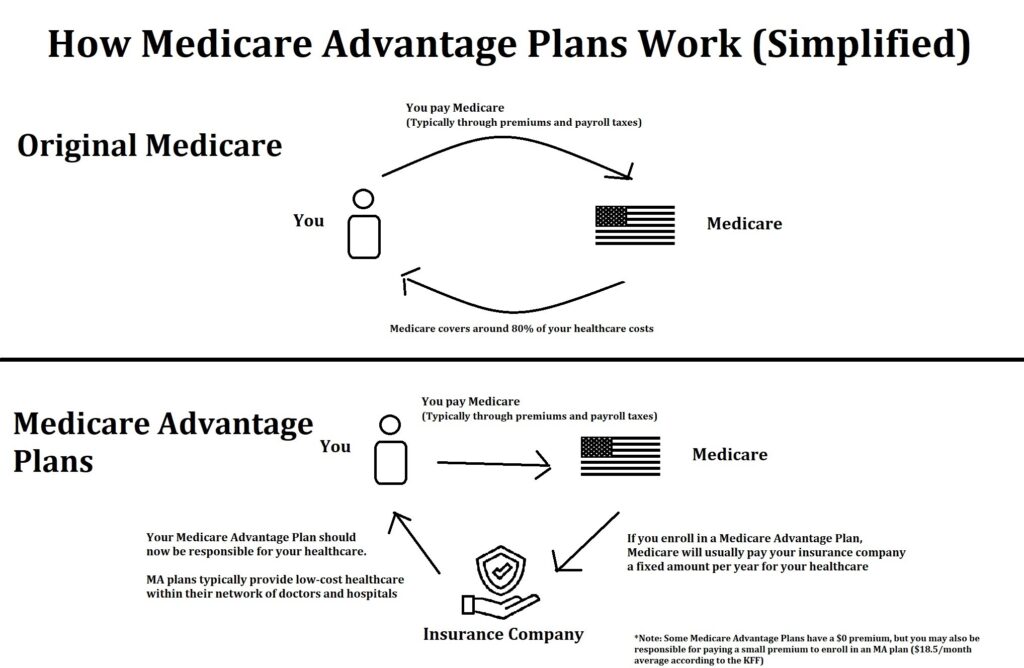

When you sign up for Medicare, you’ll usually sign up for Medicare Part A (hospital coverage) and Medicare Part B (medical coverage). Together, these two parts are called Original Medicare.

Medicare Part A has a $0 premium for most people. What catches many people off guard is that Medicare Part B isn’t the same.

Most people need to pay Medicare $202.90/month to get Medicare Part B coverage. This is the Medicare Part B monthly payment costs.

What Are Medicare Advantage Plans?

Medicare Advantage Plans, also called Medicare Part C, are plans provided by private insurance companies to help you pay for the out-of-pocket healthcare expenses that Original Medicare doesn’t cover. They have very low and often $0 premiums.

When you sign up for a Medicare Advantage Plan, Medicare will transfer the responsibility of your healthcare to the private insurance company you signed up with.

Medicare pays the insurance company a fixed amount per person per year, and the insurance company is free to decide how to use that money.

That’s why aside from covering your healthcare expenses, Medicare Advantage Plans can also offer perks like dental, vision, and hearing allowances. This is also what allows some Medicare Advantage Plans to offer the Medicare Giveback Program option, where they can help you pay for the Medicare Part B premium.

Who Qualifies for Medicare Giveback Programs?

To enroll in a Medicare Advantage Plan with this perk, you’ll typically need:

- To be enrolled in Medicare Parts A and B

- To be paying the Medicare Part B Premium

- To live in an area with a Medicare Advantage Plan that offers Medicare Giveback Programs

There are usually no special age or income requirements to get this benefit.

The most important factor is that you live in an area with a plan that offers a Medicare Giveback Program.

The Medicare Advantage Plans available to you depend on which part of the country you live in. Your options differ from state to state, and even from county to county.

So you may not have Medicare Advantage (MA) plans in your area that have this benefit. In fact, a couple years ago KFF found that 81% of Medicare Advantage Plans don’t offer a Medicare Part B Giveback Program. This isn’t a common perk.

How to Claim the Medicare Part B Giveback Perk

If you enroll in a plan with the Medicare Part B Giveback perk, you normally don’t have to do anything to enjoy it. It will usually be done automatically.

- Normally, if you’re getting Social Security, the Giveback amount will automatically be added to your Social Security check. So for example, if you’re getting $1,700 from Social Security, and your Medicare Giveback amount is $25, your Social Security check would amount to $1,725. Also, if you’re having your Medicare Part B premium deducted from Social Security, the Giveback Program should add back part of the deduction.

- If you’re not getting Social Security, your $25 Medicare Giveback amount will be automatically deducted from your Medicare Part B premium. The Part B costs $202.90/month for most people in 2026. If you have a $25 Medicare Giveback perk, your monthly payments will only be $177.90/month.

- When you first enroll in a Medicare Advantage Plan with a Medicare Giveback Program, there may be a delay from the time you sign up to when you start getting the Medicare Part B reduction. Don’t worry, because once it kicks in, it should reimburse you for the months you were covered by the plan but didn’t get the reduction.

Should You Switch Medicare Advantage Plans to Get the Medicare Giveback Program?

Most people don’t switch Medicare Advantage plans just to get the Medicare Giveback Program.

Remember, Medicare Giveback Programs are bonuses. They typically aren’t the most important deciding factor when you’re choosing which plan that meets your needs.

Pro Tip!

Be wary of Medicare Advantage Plans that have a lot of bonuses. These bonuses are not usually free. Remember, the insurance companies are getting a set amount of money from the government every year to take care of you. Having a lot of bonuses may mean that they’re choosing to spend more of the money on bonuses rather than on healthcare coverage. That’s why it helps to look at their healthcare coverage first before considering the bonuses.

What to Look For in a Medicare Advantage Plan

When you’re choosing a Medicare Advantage Plan, there are a few key details you need to check before deciding:

- Network – Most Medicare Advantage Plans have networks of hospitals and doctors. You can typically get lower-cost healthcare if you stay within your plan’s network, but you may have to pay more if you go out-of-network. Find a Medicare Advantage Plan that covers the right hospitals in your area.

- Deductibles, copays, and coinsurances – Most Medicare Advantage plans have $0 premiums. However, they may offset this by making you pay deductibles, copays, and coinsurances when you get treatment. Analyze how much these out-of-pocket expenses are.

- Max Out-of-Pocket Spending – Many Medicare Advantage Plans have a maximum out-of-pocket spending limit. This means that if your costs for copays and coinsurances reach a certain amount, you’ll no longer have to pay anything for the rest of the year. Typically, the lower the max out-of-pocket spending is, the better. Be sure to compare this with the other parts of the plan!

- Prescription Drug Plans – Medicare Advantage Plans often have drug coverage. However, it’s important to check if the drugs you take are included in these plans.

- Monthly cost – Again, most Medicare Advantage Plans have a $0 monthly payment. However, some may charge you $20/month, $50/month, or higher. It might seem small at first, but these can certainly add up over time!

- Dental, Vision, and Hearing Perks – Original Medicare typically does not cover dental, vision, and hearing care. A lot of people have trouble with these three as they get older. This is why finding a Medicare Advantage plan that offers dental, vision, and hearing care can save you money.

Other Ways to Save on Medicare Premiums

The Medicare Giveback Program is often not as great as advertisements make it seem.

Fortunately, that isn’t the only way to save money on your Medicare Part B monthly fees.

Some low-income individuals can sign up for Medicaid and their Medicare Savings Programs (MSPs) to help pay for their expenses.

According to medicare.gov there are 4 Medicare Savings Programs, or levels of Medicaid, you could potentially sign up for:

1. Qualified Medicare Beneficiary (QMB):

- Helps pay Medicare Part A premiums, Medicare Part B premiums, deductibles, coinsurance, and copayments

- With QMB, providers generally cannot bill you for Medicare-covered deductibles, coinsurance, or copayments

- Income limits (2026): Individuals — $1,350/month; Couples — $1,824/month

- Resource limits (2026): Individuals — $9,950; Couples — $14,910

2. Specified Low-Income Medicare Beneficiary (SLMB):

- Helps pay Medicare Part B premiums only

- Has higher income limits than QMB

- Income limits (2026): Individuals — $1,616/month; Couples — $2,184/month

- Resource limits (2026): Individuals — $9,950; Couples — $14,910

3. Qualifying Individual (QI):

- Helps pay Medicare Part B premiums only

- Typically has higher income limits than QMB and SLMB

- Generally, you apply every year, and applications are approved on a first-come, first-served basis

- You can’t get QI benefits if you qualify for Medicaid

- Income limits (2026): Individuals — $1,816/month; Couples — $2,455/month

- Resource limits (2026): Individuals — $9,950; Couples — $14,910

These are the 2026 federal limits for most states. Limits are higher in Alaska and Hawaii, and some states may let people qualify with higher income or resources.

4. Qualified Disabled and Working Individuals (QDWI):

- Helps pay Medicare Part A premiums only

- You may qualify if you have a disability, are working, and lost your Social Security disability benefits and premium-free Medicare Part A because you returned to work

- Income limits (2026): Individuals — $5,405/month; Couples — $7,299/month

- Resource limits (2026): Individuals — $4,000; Couples — $6,000

Note: income limits may vary depending on which state you live in!

Conclusion: Should You Get a Medicare Giveback Program?

In short:

If you find a Medicare Advantage Plan that meets your needs and happens to have a Medicare Giveback Program, then go for it!

The $202.90/month 2026 Medicare Part B premium could be heavy on your wallet. So if you can find a way to reduce that amount, that can help you afford other things in your life.

However, we recommend not making this perk the sole basis of your plan choice.

It is important to find a plan that will cover your hospital bills if you have a major illness or condition.

That’s why we say that you should treat the Medicare Giveback bonus the way it should be treated: as a bonus.

Need help finding the right plan fit for you? Give us a call or text us at +1 877-360-6565 (TTY: 711) and our team of professional licensed insurance agents will help find the right plan for your specific needs!

Calvin Bagley is the founder of PlanFit, The Medicare Store, and Nuvo Health. He and his team have helped over 60,000 people navigate Medicare options, and he’s a nationally recognized speaker in the Medicare industry. Most importantly, he’s someone who believes every American deserves clear, honest information without pressure.