Medicare is complex enough to confuse even the brightest people—and to make matters worse, most people only get one six-month period where they can enroll in a Medicare Supplement Plan without medical underwriting.

This means it’s important to make the right decision for you from the get-go.

You’ve likely seen many online licensed insurance salespeople recommending Medicare Supplement Plans. But is that really the best option for you?

Medicare Supplement Plans are typically more expensive than your other options. They also don’t cover prescription drugs, and routine dental, vision, and hearing care.

But despite the higher costs, you’ll often find people praising Medicare Supplement Plans, and encouraging others to enroll.

While there are clear advantages to a Medicare Supplement Plan, you also deserve to know that many of the agents who try to sell them to you, are only doing so because it’s good for their bank account.

If you’re at a crossroads trying to decide between enrolling in a Medicare Supplement and Medicare Advantage Plan, you need to be aware that many agents don’t have a license to sell Medicare Advantage.

Because of this, they’ll try to push you into a Medicare Supplement Plan.

The best way for you to ensure you’re getting a plan that fits your needs will always be to do your own research.

That’s why in this article, we’ll explore everything you need to know about Medicare Supplement Plans. We’ll take a look at how they work, your plan options, three reasons to choose a Medicare Supplement Plan, and three reasons why you might consider another type of plan instead.

By the end of this article, you should have a much better idea of whether a Medicare Supplement Plan is the right fit for your situation.

What Are Medicare Supplement (Medigap) Plans?

Medicare Supplement Plans are secondary insurance to Original Medicare provided by private insurance companies. They help cover your out-of-pocket expenses with Original Medicare.

With Original Medicare (Medicare Part A and B), there are several out-of-pocket expenses that you are responsible for paying. Generally speaking, Medicare pays around 80% of your costs, while you pay the remaining 20%, with no cap on how much you can spend.

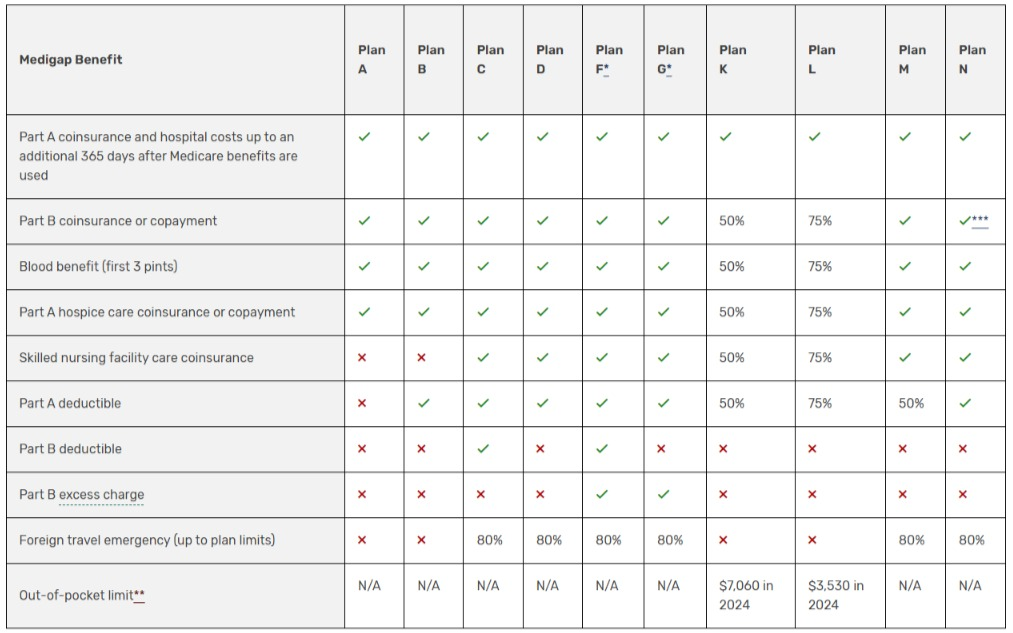

Medicare Supplement Plans help reduce this out-of-pocket spending with Original Medicare. There are ten standardized Medicare Supplement Plans today (namely Plan A, B, C, D, F, G, K, L, M, and N), and each plan type provides the same coverage regardless of which insurance company you purchase the plan from.

Note: Medicare Supplement Plans are also called Medigap Plans. These two are the same thing.

What Do Medicare Supplement Plans Cover?

There are generally six gaps in Medicare that Medicare Supplement Plans cover (depending on the plan type). These are:

- Medicare Part A Deductible: Medicare Part A has a deductible that you have to spend out-of-pocket first before you get coverage. In 2024, the Medicare Part A deductible is set to $1,632 per benefit period. Some Medicare Supplement Plans cover this deductible for you.

- Medicare Part A Hospital Copays: If you’re admitted to a hospital for over 60 days, Medicare Part A will start charging you daily copays. In 2024, this costs $408/day for days 61-90, $816/day for days 91-150 (using lifetime reserve days), and after day 150, you pay 100% of the bill. All ten Medicare Supplement Plans today cover these daily hospital copays.

- Skilled Nursing Facility (SNF) Copays: If you’re admitted to a skilled nursing facility for more than 20 days, you’re responsible for paying daily copays ($204/day for days 21 – 100, and 100% of costs after day 100 in 2024). Some Medicare Supplement Plans will cover these daily SNF copays for you.

- Medicare Part B Deductible: Like Medicare Part A, Medicare Part B also has a deductible before it starts covering your medical needs. In 2024, the Medicare Part B deductible is set to $240. Medicare Supplement Plans F and C cover the Part B deductible. However, these two Medicare Supplement Plans are no longer available to people who turn 65 after January 1, 2020.

- Medicare Part B Coinsurance: Medicare Part B only pays 80% for most covered items and services, and you’re usually responsible for paying the remaining 20% out-of-pocket. However, most Medicare Supplement Plans will pay this 20% coinsurance for you instead.

- Medicare Part B Excess Charges: Most healthcare providers that take Medicare also accept the Medicare-approved amount as payment. However, there are a few who may charge up to 15% more than the Medicare-approved amount, and you are responsible for paying this excess charge 100% out-of-pocket. Some Medicare Supplement Plans will cover these excess charges for you should they come up.

- First Three Pints of Blood: If you have to purchase blood, Original Medicare doesn’t cover the first three pints. However, most Medicare Supplement Plans will cover this for you.

Here’s a quick chart of what each Medicare Supplement Plan type covers:

How Much Do Medicare Supplement Plans Cost?

The monthly premium of Medicare Supplement Plans depends on several factors including the plan type, your age, whether you use tobacco or not, whether you qualify for household discounts, and several other factors. The price of Medicare Supplement Plans also varies widely from location to location.

To help you get a better idea of how much Medicare Supplement Plans cost, here’s the price range for Medicare Supplement Plan G and Plan N (two of the most popular Medicare Supplement Plans) taken from different cities across the United States.

Note: to find out how much Medicare Supplement Plans cost in your area, you may call or text us at +1 877-360-6565 (TTY: 711). Our team of licensed insurance agents would be glad to provide accurate quotes at no cost to you!

| Medicare Supplement Plan G | Medicare Supplement Plan N | |

| New York City, New York | $302 – $776 | $220 – $483 |

| Indianapolis, Indiana | $114 – $493 | $86 – $496 |

| Los Angeles, California | $148 – $278 | $114 – $213 |

*Price estimates above are taken from Medicare.gov for a 65-year-old male who doesn’t use tobacco and doesn’t qualify for household discounts. To get accurate quotes in your area, contact us at +1 877-360-6565 (TTY: 711)

3 Reasons to Consider a Medicare Supplement Plan

Now that you know what Medicare Supplement Plans are, what they cover, and how much they cost, let’s take a look at some of the reasons some people prefer Medicare Supplement Plans.

#1: Standardized Plans

| Medicare Supplement | Medicare Advantage |

| 10 standardized plans to choose from. All insurance companies must provide the exact same coverage for each of these plans | No standardized plans. Insurance companies can decide how much or how little they cover |

| Coverage will NEVER change | Coverage changes every year |

One reason some people prefer Medicare Supplement Plans over Medicare Advantage Plans and other insurance is because Medicare Supplement Plans are standardized by Medicare.

Medicare Supplement Plans don’t change their coverage every year. Once you enroll in a Medicare Supplement Plan, your coverage will remain the same as long as you have the plan. This is unlike most Medicare Advantage Plans, where the coverage changes every year.

Regulation changes sometimes prevent new enrollees from joining some Medicare Supplement Plans—such as Medicare Supplement Plan J in 2010, or Medicare Supplement Plan F, which is currently only available for people who turned 65 before January 1, 2020. However, regulation changes are usually few and far between, and the people who already had those plans when these regulation changes were passed are still allowed to keep the plan.

That’s why people who don’t want to review their coverage every year often prefer Medicare Supplement Plans.

#2: No Networks

| Medicare Supplement | Medicare Advantage |

| Get coverage for any doctor or hospital that accepts Medicare | Get coverage only for doctors and hospitals within insurance company’s network |

| Covered in hospitals all over the country | Most networks are location-based, meaning you usually won’t have coverage outside your county |

| No referrals and prior authorizations | Referrals and prior authorizations are required before insurance covers treatment |

If you enroll in a Medicare Supplement Plan, you won’t have to worry about staying in your plan’s network of doctors and hospitals. With a Medicare Supplement Plan, you’ll get coverage for any healthcare provider in the country that accepts Medicare.

With a Medicare Supplement Plan, you typically don’t require referrals or prior authorizations from your insurance company before you can get coverage for special treatment. Usually, if your doctor deems a procedure “medically necessary” your Medicare Supplement Plan should cover it.

Meanwhile, Medicare Advantage Plans usually have networks of doctors and hospitals where their enrollees can get low-cost healthcare. However, some Medicare Advantage Plans won’t cover enrollees if they go out-of-network (except in emergencies), while some PPO plans will charge higher copays for out-of-network services.

Some Medicare Advantage Plans may also require referrals to see a specialist or prior authorizations for expensive treatment.

That’s why people who live in areas where Medicare Advantage Plans don’t have many in-network options often prefer Medicare Supplement Plans. Some people also enjoy the flexibility that Medicare Supplement Plans give them.

#3: Predictable Costs

| Medicare Supplement Plan G | Medicare Advantage |

| Higher premiums but predictable costs all year round | Lower premiums but out-of-pocket costs can get significantly higher than Plan G if you need many treatments |

Another reason why some people prefer Medicare Supplement Plans is their more predictable costs. In general, Medicare Supplement Plans have higher premiums, but lower out-of-pocket expenses. In contrast, Medicare Advantage Plans have lower to $0 premiums, but higher and less predictable out-of-pocket expenses.

For example, if you enroll in a Medicare Supplement Plan G (one of the most popular Medicare Supplement Plans today), your healthcare costs for the year will typically only be:

- Medicare Part A Premium = $0 for most people

- Medicare Part B Premium = $174.7/month in 2024

- Medicare Supplement Plan G Premium = Varies (call or text us at +1 877-360-6565 (TTY: 711) for quotes in your area)

- Medicare Part B Deductible = $240 in 2024 (this is one of the few out-of-pocket expenses that Medicare Supplement Plan G doesn’t cover)

Once you pay those four items, Medicare Supplement Plan G should cover most of your other healthcare costs. However, it does not yet cover prescription drugs. Most people who enroll in a Medicare Supplement Plan also enroll in a standalone Medicare Part D prescription drug plan, which has its own set of costs.

However, even with the costs of a standalone Medicare Part D prescription drug plan, enrolling in a Medicare Supplement Plan (especially Plan G) provides enrollees with much more predictable costs than a Medicare Advantage Plan—which usually has different copays for different types of services.

Pro Tip!

You can compare the costs of a Medicare Supplement Plan to that of a buffet restaurant, and the costs of a Medicare Advantage Plan to that of an ala carte restaurant.

Buffets cost more upfront, but you can eat as much as you’d like without paying extra. A la carte is cheaper if you only order a few dishes, but can get more expensive the more you order.

3 Reasons Not to Consider a Medicare Supplement Plan

There are several reasons why people choose not to enroll in a Medicare Supplement Plan. Here are three of the most common ones:

#1: No Dental, Vision, and Hearing Care

| Medicare Supplement | Medicare Advantage |

| Dental, vision, and hearing care NOT included | Many plans have allowances for dental, vision, and hearing care |

Because Medicare Supplement Plans are secondary insurance to Original Medicare, they don’t provide any additional coverage. If Medicare doesn’t cover an item or service, Medicare Supplement Plans won’t cover it as well (one big example of this is most prescription drugs).

That’s why people who choose to enroll in a Medicare Supplement Plan often have to enroll in a separate Medicare Part D prescription drug plan, as well as find other ways to cover their routine dental, vision, and hearing care.

Not only will you need separate cards for Original Medicare, your Medicare Supplement Plan, your Medicare prescription drug plan, and any other insurance you enroll in for coverage, but the cost of premiums for all of these can add up.

Contrast that to Medicare Advantage Plans, which you can think of as an all-in-one plan. Medicare Advantage Plans include everything in Original Medicare and usually have a built-in prescription drug plan, and many Medicare Advantage Plans also have allowances for dental, vision, and hearing care.

#2: May Require a Medical Underwriting Process

| Medicare Supplement | Medicare Advantage |

| ONE Open Enrollment Period (6 months after you turn 65) | 2 enrollment periods every year |

| Medical underwriting process if you enroll outside the Open Enrollment Period | No medical underwriting process |

| Very difficult to switch between Medigap plans | Very easy to switch between Advantage plans every year |

Most Medicare Supplement Plans will have a medical underwriting process before you can enroll. This is a set of health-related questions to determine if you qualify for the plan or not. If you have a pre-existing condition, you may be declined from enrolling in a Medicare Supplement Plan, or you may be charged higher premiums.

However, everyone gets one Medigap Open Enrollment Period when Medicare Supplement Plans must take you in regardless of your health condition. This is known as the Medigap Open Enrollment Period, and it runs for six months starting when your Medicare Part B coverage begins.

If you enroll during your Medigap Open Enrollment Period, insurance companies selling Medicare Supplement Plans cannot have a medical underwriting process, they must take you in, and they cannot charge you more than the preferred rate for the plan.

However, once your Medigap Open Enrollment Period is over, you generally have to undergo a medical underwriting process to enroll in a Medicare Supplement Plan.

This is unlike Medicare Advantage Plans, which have no medical underwriting process whatsoever. You also get the Annual Enrollment Period (AEP) every October 15 – December 7 where you can enroll in or switch your Medicare Advantage Plan. There’s also the Medicare Advantage Open Enrollment Period that runs from January 1 to March 31 every year and allows people to switch between Medicare Advantage Plans.

This is why switching to or between Medicare Supplement Plans can be difficult, whereas switching to or between Medicare Advantage Plans is relatively easy.

#3: Premiums Go Up Every Year

| Medicare Supplement | Medicare Advantage |

| High premiums | Low to zero premiums |

| Premiums go up as you get older | Premiums generally stay the same |

Not only are Medicare Supplement Plans generally more expensive than Medicare Advantage Plans, but their premiums also tend to go up as you age.

The coverage of Medicare Supplement Plans doesn’t change, but their prices tend to go up every year. The cost of a Medicare Supplement Plan G when you’re 65 is usually lower than it will cost you when you turn 70, 75, or 80.

That’s why people should know that if they find a Medicare Supplement Plan is too expensive for them at 65, it will usually only get more expensive as the years go by.

Pro Tip!

Here’s an example: if your Medicare Supplement Plan G costs $150/month when you’re 65, this can go all the way up to $300/month by the time you turn 80. That’s why it’s important to consider rising prices if you choose to go for a Medicare Supplement Plan.

However, the actual cost of Medicare Supplement Plans when you’re 65 compared to when you’re 80 varies widely. For accurate quotes in your area, call or text us at +1 877-360-6565 (TTY: 711)

Should You Get a Medicare Supplement Plan?

In Medicare, there is no such thing as the “best” plan. There is only the right plan fit for YOU. We hope that this article helps you understand Medicare Supplement Plans, and helps you decide whether or not this is the right fit for you.

Before we go, here’s a quick chart of some choices that we commonly see people making:

| Choices We Commonly See | |||

| High Income | Average Income | Low Income | |

| Few Health Issues | Medigap Plan G | Medigap Plan N or Medicare Advantage (PPO) | Medicare Advantage (HMO) |

| More Health Issues | Medigap Plan G | Medigap Plan G | Medicare Advantage (HMO) or Medicaid |

Very generally speaking, people with high income tend to choose Medicare Supplement Plan G. High-income earners can afford the higher premiums, as well as the costs for the other plans they enroll in (such as Medicare Part D prescription drug plans, and plans for dental, vision, and hearing care).

We also see many people on average income who have few health issues choose a Medicare Supplement Plan N or a Medicare Advantage PPO plan. Medicare Supplement Plan N generally has lower monthly premiums than Plan G, but more copays. This is why some people who aren’t expecting to see the doctor a lot choose this plan to save some money. We also see some average-income people with few health issues opt for a Medicare Advantage PPO plan, which is more flexible than HMO plans but typically has higher copays.

Average-income earners who have many health issues sometimes choose a Medicare Supplement Plan G. This is because even though Medicare Supplement Plan G premiums can be expensive for average-income earners, the low out-of-pocket expenses may make it worth it for them.

Finally, we see many low-income earners choosing a Medicare Advantage HMO Plan. This is because Medicare Advantage HMO plans usually have the lowest premiums. Depending on how much they earn, low-income earners may also qualify for Medicaid, which is a joint federal and state program that helps people below the poverty line pay for their medical costs.

Again, keep in mind that these are example situations.

The right plan fit for you will depend on the plans available in your area, and your unique needs. That’s why if you want help finding the right plan for you, call or text our team of licensed insurance agents at +1 877-360-6565 (TTY: 711), and we’d be happy to assist at no cost to you!

Calvin Bagley is the founder of PlanFit, The Medicare Store, and Nuvo Health. He and his team have helped over 60,000 people navigate Medicare options, and he’s a nationally recognized speaker in the Medicare industry. Most importantly, he’s someone who believes every American deserves clear, honest information without pressure.